Debt Management Program Survey: Over Half Don’t Get Help Until They Owe Five Figures

Americans are carrying near-record credit card debt — $1.25 trillion according to the latest Federal Reserve Bank of New York report — and even though they know they need help, they admit they wait until the last minute to ask for it.

To understand how Americans are navigating that debt, Consolidated Credit surveyed 1,005 U.S. adults about their credit card balances, their awareness of debt relief options, and what stands in the way of getting help.

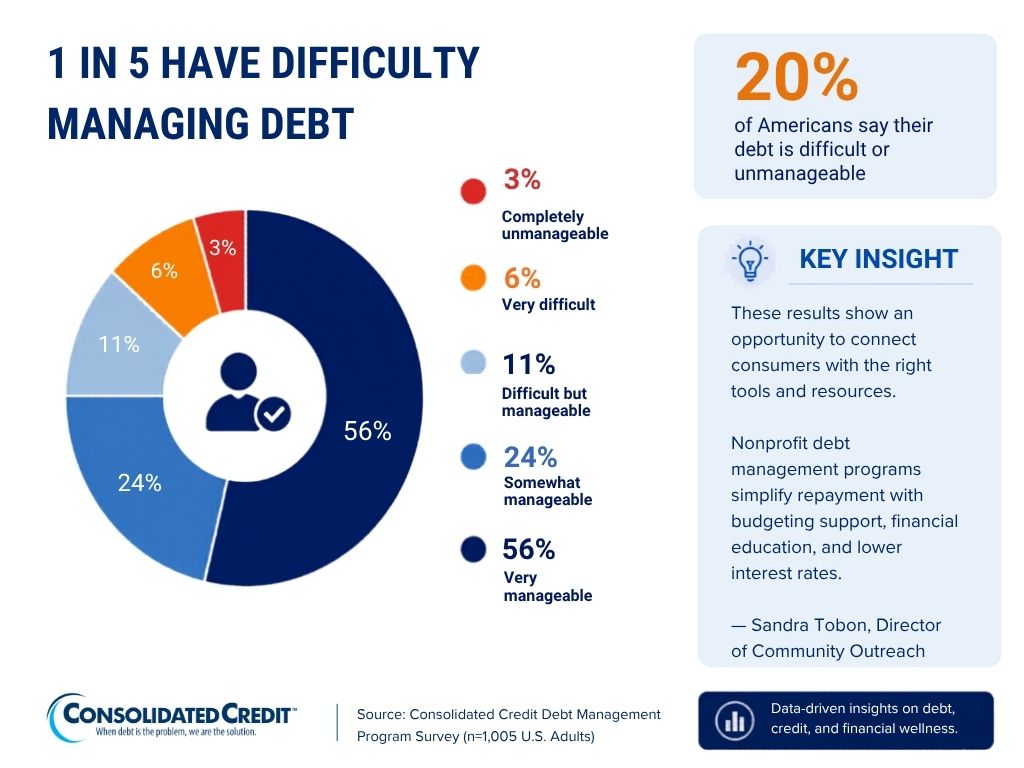

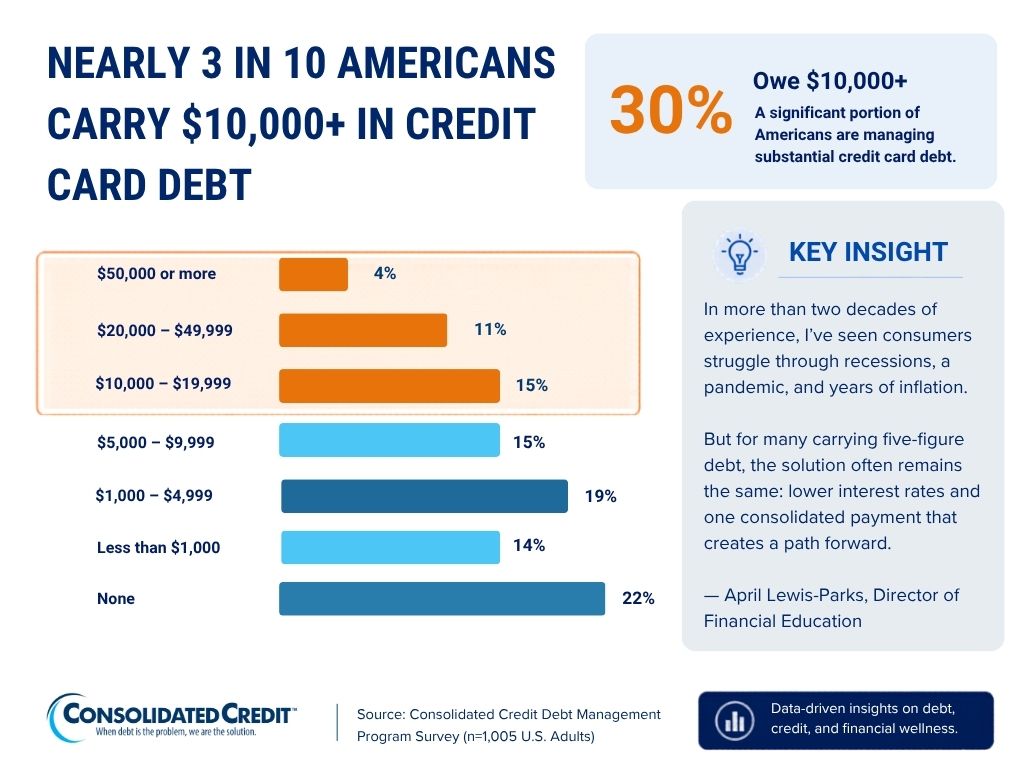

The survey found that 78% of respondents carry credit card debt, including 30% who owe $10,000 or more. Despite those balances, most describe their debt as manageable, which may help explain why many delay seeking help.

While familiarity with common debt relief options is relatively high, fewer respondents understand how Debt Management Programs work or when to use them, and concerns about cost, credit impact, and repayment time continue to shape decisions — even among those who say they trust nonprofit credit counseling agencies.

Key findings

- 78% of respondents carry credit card debt, and 30% owe $10,000 or more.

- About 1 in 5 say they would delay seeking help until it is a last resort, while 6% would never seek help.

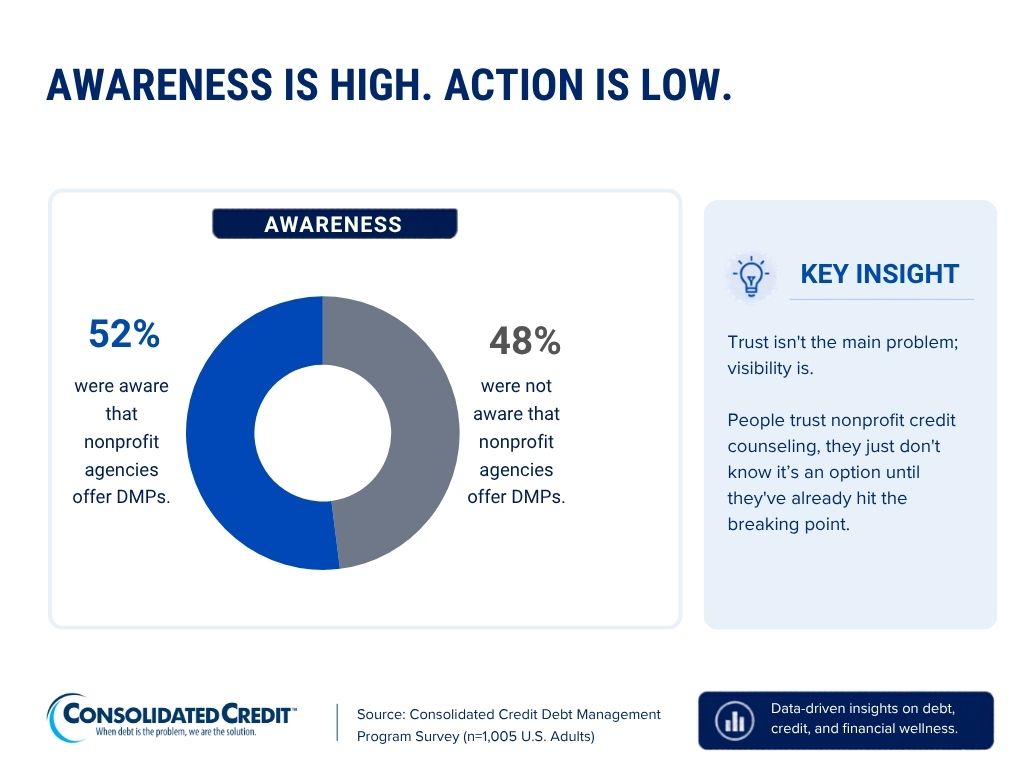

- Nearly half (48%) were not aware that nonprofit agencies offer Debt Management Programs.

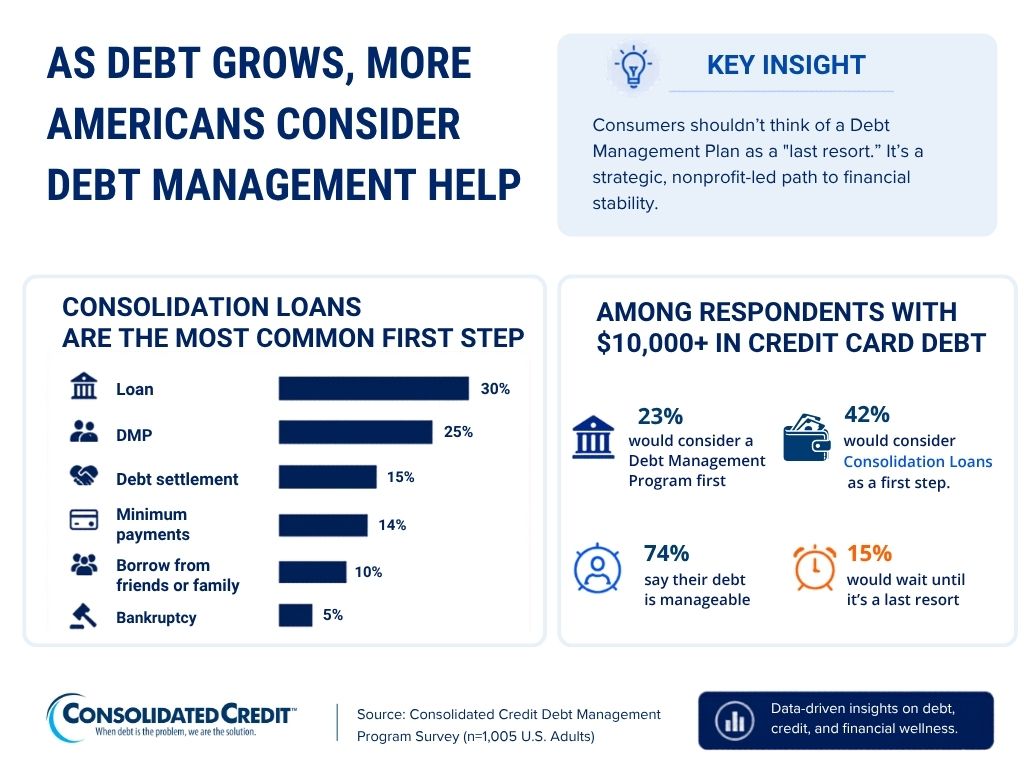

- Debt consolidation loans are the most common first step, ahead of Debt Management Programs –– only 37% have even heard of a DMP.

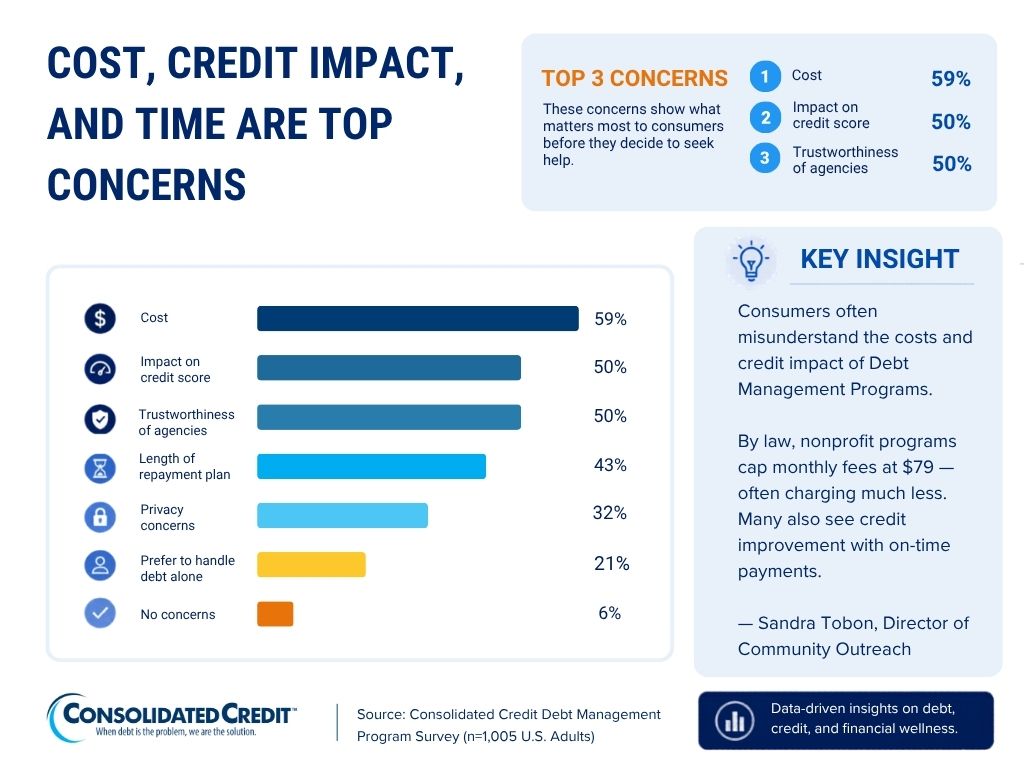

- Cost, credit impact, and repayment time are the most common concerns about enrolling

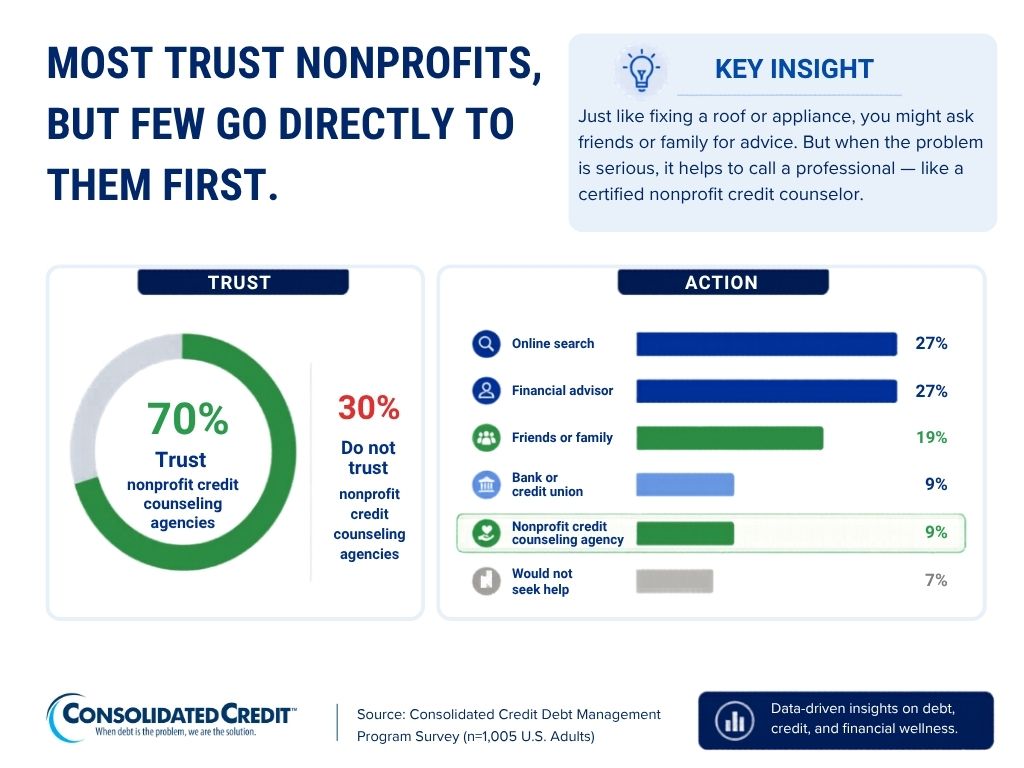

- 70% say they trust nonprofit credit counseling agencies, but few say they would turn to one first.

- Only 39% say they have enrolled in a Debt Management Program.

Responses show a clear pattern of delayed action. Only a small share would consider help at lower debt levels, while interest in help increases as balances grow.

More notably, a significant portion of respondents indicate they would only seek help as a last resort or not at all. This suggests that for many borrowers, professional guidance is viewed as a reactive step rather than a proactive one.

Credit card debt is not evenly distributed, but higher balances are not uncommon. While smaller balances make up a large portion of responses, more than a quarter of respondents report debt levels that typically take years to repay.

At the same time, these higher balances do not necessarily translate into urgency. Many respondents with five-figure debt still describe their situation as manageable, suggesting that perception may not always align with financial risk.

More widely marketed or commonly discussed options, such as consolidation loans and bankruptcy, are more familiar to respondents.

One in four say they’ll consider a Debt Management Program as their first step for help with their debt. Even when faced with $10,000 or more in credit card debt, 23% consider a DMP to guide them on a path to financial stability.

Trust does not appear to be the primary barrier. While most respondents say nonprofit agencies are trustworthy, far fewer say they would actively seek them out.

Many start by researching online and consulting personal networks, suggesting a gap in visibility rather than credibility.

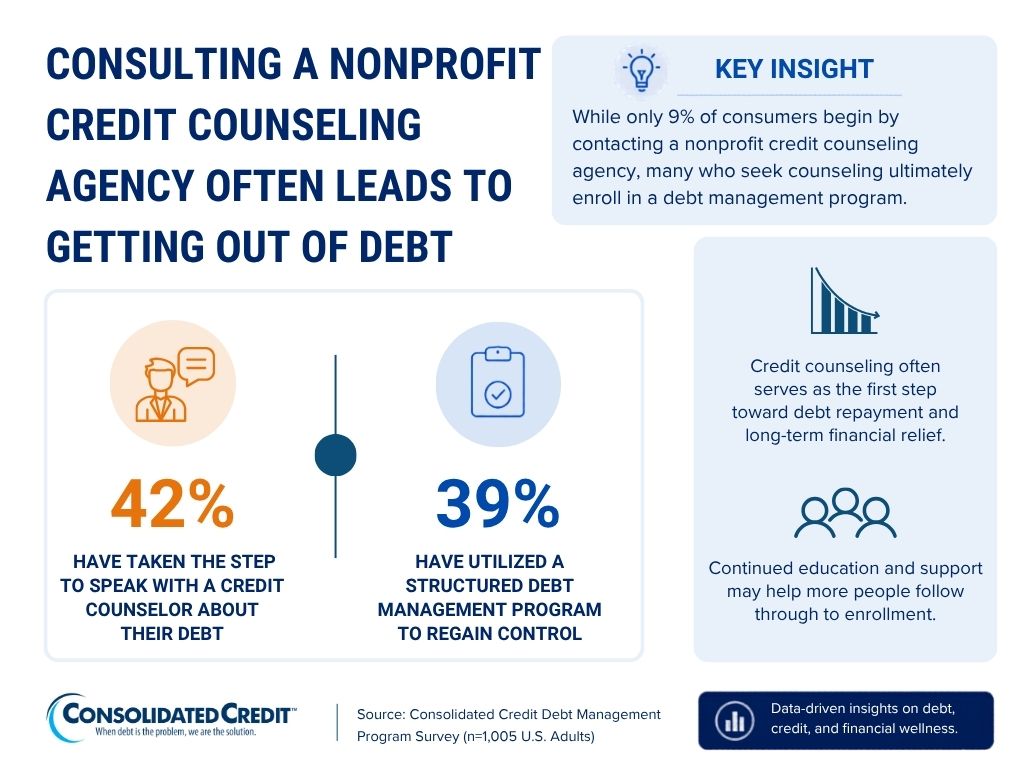

Engagement with credit counseling is not uncommon, but a majority of respondents have not taken that step. A small amount said they would directly contact a nonprofit credit counseling agency for debt help.

However, 4 in 10 say they have taken the step to speak with a credit counselor. Then 39% have enrolled in a Debt Management Program, reinforcing the benefits of nonprofit credit counseling agencies and their financial resources, guidance, and tools.

This lack of awareness represents a meaningful barrier. For borrowers who may be hesitant to work with for-profit companies, not knowing that nonprofit options exist could limit their willingness to seek help.

It also suggests that awareness of the program itself and awareness of who offers it are separate challenges. But for the more than half that are aware nonprofits offer Debt Management Programs is a positive sign consumers can take control of their financial health.

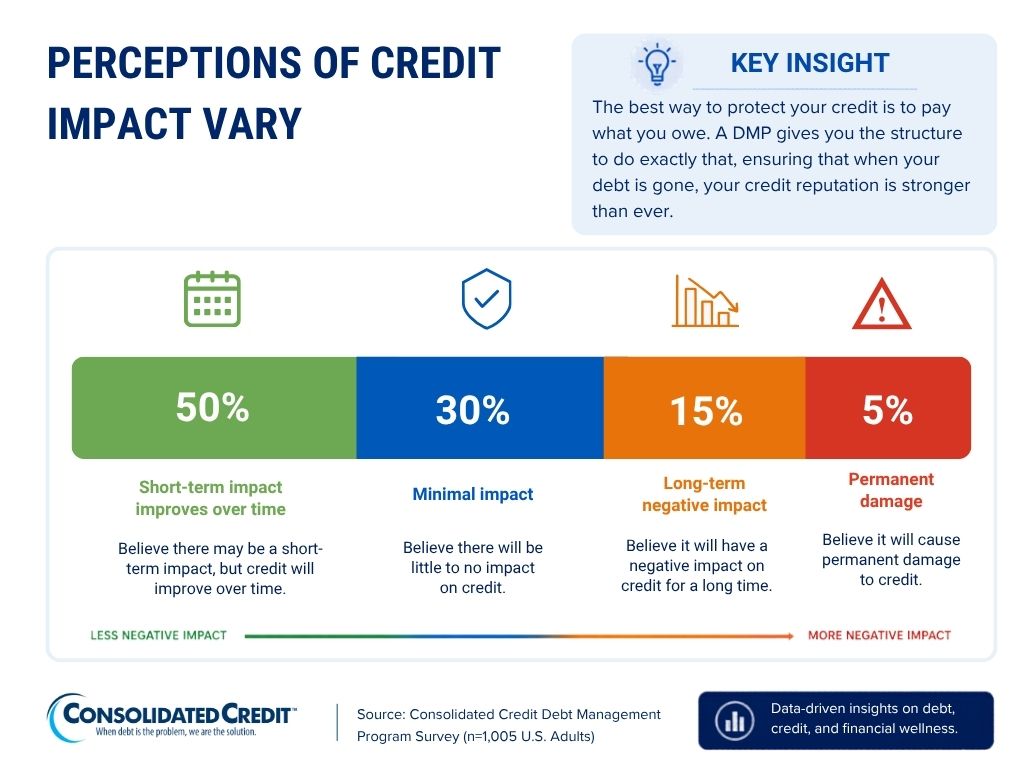

Misconceptions about how Debt Management Programs work are common. A significant share of respondents assume negative long-term credit outcomes. Many consumers report positive impact to their credit profile after making consistent on-time payments to their creditors through a program.

That credit confusion may contribute to hesitation and delay in decision-making. While many respondents expect some short-term impact, others believe the effects could be long-lasting or permanent.

Concerns about enrolling in a Debt Management Program are largely practical. Cost, credit impact, and repayment length all rank highly, suggesting that borrowers are focused on how a program will affect them in the short term.

Fees for a Debt Management Program are typically between $0-$79, depending on the state the agency is located in. But fees are capped at $79 nationwide. So consumers will never pay more than that no matter where in United States they’re located.

| Approximately how much credit card debt do you have? | |

|---|---|

| None | 22.29% |

| Less than $1,000 | 14.43% |

| $1,000-$4,999 | 19.10% |

| $5,000-$9,999 | 14.63% |

| $10,000-$19,999 | 14.53% |

| $20,000-$49,999 | 11.44% |

| $50,000 or more | 3.58% |

| How manageable does your current debt feel? | |

|---|---|

| Very manageable | 55.52% |

| Somewhat manageable | 24.28% |

| Difficult but manageable | 10.85% |

| Very difficult to manage | 5.97% |

| Completely manageable | 3.38% |

| At what point would you consider seeking professional help for debt? | |

|---|---|

| Less than $5,000 in debt | 7.86% |

| $5,000-$9,999 | 12.24% |

| $10,000-$19,999 | 19.50% |

| $20,000-$49,999 | 19.00% |

| $50,000 or more | 14.43% |

| I would only seek help as a last resort | 21.09% |

| i would never seek help | 5.87% |

| Which of the following debt relief options have you heard of (Select all that apply) | |

|---|---|

| Debt consolidation loan | 69.15% |

| Debt settlement company | 53.63% |

| Bankruptcy | 58.01% |

| Debt Management Program | 36.92% |

| Balance transfer credit card(s) | 45.27% |

| I have not heard of any of these | 6.67% |

| Before today, how familiar were you with Debt Management Programs? | |

|---|---|

| Very familiar | 34.23% |

| Somewhat familiar | 32.64% |

| Not familiar at all | 33.13% |

| Before today, did you know nonprofit credit counseling agencies offer Debt Management Programs? | |

|---|---|

| Yes | 51.64% |

| No | 48.36% |

| If you were struggling with debt, which solution would you most likely consider first? | |

|---|---|

| Debt consolidation loan | 30.05% |

| Debt settlement program | 15.32% |

| Debt management program | 24.88% |

| Bankruptcy | 5.37% |

| Borrow money from friends or family | 9.95% |

| Continue making minimum payments | 14.43% |

| Which of the following statements best reflects what you believe about Debt Management Programs? | |

|---|---|

| They help people repay debt in full over time | 49.95% |

| They reduce or eliminate debt owed | 31.74% |

| They damage your credit long-term | 6.47% |

| They are risky or too good to be true | 11.84% |

| How do you think a Debt Management Program affects your credit score? | |

|---|---|

| Minimal, because your debts are paid in full at the end of the program | 30.35% |

| Your credit score may be reduced in the short term, but will improve over time as you make on-tme payments | 50.25% |

| Your credit score will be lowered and remain low for years | 14.63% |

| It will damage your credit permanently and you won’t be able to get credit again | 4.78% |

| What concerns would make you hesitate to enroll in a Debt Management Program? (Select all that apply) | |

|---|---|

| Cost of the program | 59.20% |

| Impact on my credit score | 49.85% |

| Length of repayment plan | 42.69% |

| Trustworthiness of agencies | 50.15% |

| Privacy concerns | 32.04% |

| I prefer to handle debt on my own | 20.50% |

| I have no concerns | 5.57% |

| Do you believe nonprofit credit counseling agencies are trustworthy? | |

|---|---|

| Yes | 70.05% |

| No | 29.95% |

| Have you ever spoken with a credit counselor about your debt? | |

|---|---|

| Yes | 42.49% |

| No | 57.51% |

| Have you ever enrolled in a Debt Management Program? | |

|---|---|

| Yes | 38.81% |

| No | 61.19% |

| If you were struggling with debt, how likely would you be to seek help from a nonprofit credit counseling agency? | |

|---|---|

| Very likely | 38.41% |

| Unlikely | 35.82% |

| Likely | 25.77% |

| Where would you most likely look for help with debt? | |

|---|---|

| Online search | 26.87% |

| Financial advisor | 27.06% |

| Friends or family | 18.81% |

| Social media | 2.79% |

| Bank or credit union | 8.86% |

| Nonprofit credit counseling agency | 8.96% |

| I would never seek help | 6.67% |

Methodology: Consolidated Credit surveyed 1,005 U.S. adults age 18 and older about their credit card debt, awareness of debt relief options, and perceptions of Debt Management Programs. Respondents were from all 50 states and Washington, DC, and were aged 18 and above. Responses were collected through SurveyMonkey. The survey was conducted on April 7, 2026.