Youth Financial Literacy Resource Center

Helping kids and teens learn the skills they need for financial independence

“Financial literacy” is the ability to understand key money and credit lessons so you can use them in your daily life. Basic skills like budgeting, saving money, and using credit are essential for financial independence. These resources can help you get there!

Money and Credit Guides

These guides are a great jumping-off point to learn about personal finance. They walk you step-by-step through key financial topics that matter in your life right now. Learning these lessons now will set you up for financial success later in life.

My First Budget

Budgeting for Kids and Teens

Do you have money goals or things you want to buy? Then you need a budget! Learn what a budget is and how to build one step by step.

LEARN TO BUDGET

Banking 101

Learn about Basic Accounts

Getting your own checking and savings account is a key step to gain financial independence. Learn how to use these accounts.

GET BANKING

Credit Card Statements

Credit Card Statements

Don’t skip looking at your monthly credit card statements. It’s essential to track what’s happening with your cards.

LEARN WHAT IT SAYSBudgeting and Saving Worksheets

When it comes to managing your money, trying to “keep it all in your head” just doesn’t work. You need to write things out if you want to be successful. These downloadable worksheets can help!

Wise Up for Teens Interactive Course

Wise Up for Teens is an interactive financial literacy course that will teach you all the skills you need to be financially independent. You’ll learn how to:

- Make a budget

- Save money

- Manage your money

- Use credit wisely

Each lesson includes helpful worksheets that will guide you through each topic and a quiz to make sure you have mastered each topic.

Get wise to the ways of finance »

Be Smart About Credit Cards

Credit cards are great tools that can help you achieve your goals when used correctly. But they can also ruin your financial life if you’re not careful! The credit professor will teach you everything you need to know to use credit cards wisely.

Good Credit Habits of Smart Spenders

Credit cards are a great financial tool when used correctly. But you have to be a Smart Spender when it comes to using credit the right way.

Smart Spenders aren’t going out to get credit just because they can. And they don’t treat credit like money that they don’t have to pay back. They understand that credit cards can be used for convenience, safety and tracking, but even credit cards used for the right reasons have to be used responsibly.

Smart Spenders aren’t constantly going out and signing up for new credit cards. Instead they only get new credit when they need it and shop around for the best cards for their needs. Instead of being lured in by advertising, they research credit cards carefully to ensure they’re not blindsided once the card is in use or that the rewards aren’t worth the interest and fees.

Smart Spenders aren’t using luck or crossing their fingers hoping that they get approved because they know exactly how creditors judge creditworthiness. They understand the three Cs – character, capital and capacity. They know they have to show they’re a responsible borrower who can and will repay what they borrow, with assets to back them up.

Once Smart Spenders find the right card for their needs, they take time to read through the contract carefully so they know what they’re really getting into. They know their credit limits, can strategically pay around the grace period, and know how to avoid penalties – and exactly what those penalties will be if the card is misused.

Even though credit card statements always come with a minimum payment requirement, Smart Spenders always pay more than the minimum – it’s a trap. They usually pay off everything in full on credit cards used that month. This way they always start the month with zero balances on their cards. When they can’t pay off a balance in full, they make a plan to pay it off as fast as possible, and know how to read statements to find balance payoff information.

A credit card grace period is the amount of time you have to pay off a balance before interest charges are applied. A Smart Spender knows when the grace period ends in relation to each billing cycle so they can pay off the debt accrued that month before the interest charges are applied to minimize the cost of using credit.

Smart Spenders understand that just because a credit card company gives you a high credit limit, it doesn’t mean you should run up that debt. Smart Spenders check two metrics often: how much they can afford to borrow and what they can comfortably pay to eliminate debt each month. They check how much they can borrow by setting a limit at 15% of their net annual income. And they also check how much they can afford to pay back each month by calculating 10% of their net monthly income. This helps ensure Smart Spenders have enough money for bills, expenses like groceries, and even savings.

One of the biggest downsides to using credit is it makes it really easy to give into impulse buys when you see something you want in a store. Smart Spenders resist the temptation and only buy things when they need them after taking time to shop around for the best price. They may even think about it a few days before deciding to buy something to make sure they really have to have it. They also avoid other bad habits, like using credit to cover budget gaps, leaving balances to accrue interest month after month and using one credit card to pay another.

Now you know these eight credit habits to make you a Smart Spender, too!

-

Now PlayingGood Credit Habits of Smart Spenders

Now PlayingGood Credit Habits of Smart Spenders -

Up NextHow to Compare Credit Cards

-

Using Credit Responsibly

-

Credit Tips to Live By

A Video Guide to Good Credit

A good credit score is essential when you’re an adult. Learning how credit scores and credit reports work now will make it easier to achieve a high score. Watch these videos to learn everything you need to know!

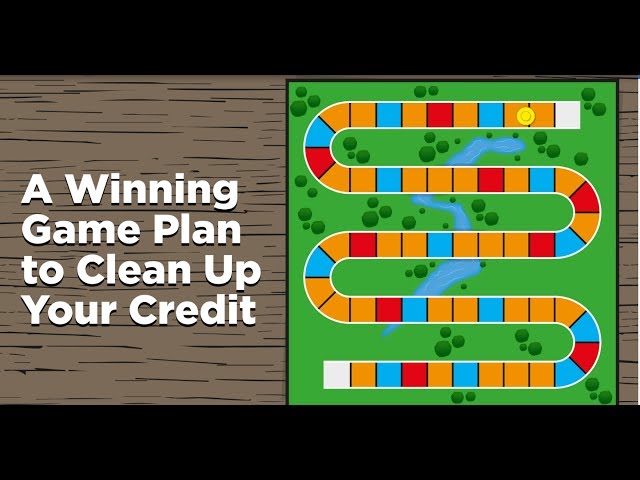

Game of Good Credit: Your Credit Score

Come on down! You’re the next contestant on the Game of Good Credit!

Achieving good credit is a game of strategy. You have to play tactically if you want to win.

Let’s begin with the basic gameplay of how to go from the starting point to winning the game of good credit so you can maximize your credit score. The overall goal in the game is to move forward from the starting point, taking the right steps to reach your credit goal.

Each step you take can have a positive, negative or neutral effect. You want to make smart moves that boost your score, while avoiding traps that set you back. Positive actions like making payments on time and keeping your credit utilization low help move you forward. And doing things like paying off a credit card in full can give you a big jump up the board. But actions like paying late or allowing an account to go into collections can set you back and put you farther away from your credit score goal.

As you play the Game of Good Credit, keep in mind that even if you have to make a really bad move it doesn’t mean you’ll have bad credit forever. You may just have to start again to begin moving forward toward the score you want. Most negative actions set you back for 7 years. Although some things like Chapter 7 bankruptcy can set you back longer. But if you have a setback, you can start to move forward immediately!

The BEST move you can make is to pay your bills on time – this is the biggest factor in calculating your score. Each time you pay a credit card or loan on time it’s a positive action that lets you move forward. If you’ve had setbacks, start making payments on time to move forward again. But keep in mind that the amount of credit you use affects how quickly you can move up the board.

Credit utilization is the second biggest factor in calculating credit scores – that’s the amount of debt you have relative to your total available credit. The less debt you have, the faster you can advance towards better credit. So by keeping your debt low and making payments on time you can forward to get closer to your credit goal.

Length of credit history is the third biggest factor in your score – creditors believe people who have been playing the game longer are better at it. So don’t close your oldest accounts or let creditors close them due to inactivity, because this can actually set you back. Keep accounts in good standing and you’ll get an extra boost on your way to a winning credit score.

The number of times you apply for new credit within a six month period is a factor in your credit score. If you try to take too many new credit moves at once, you can actually get set back. Only draw a new loan or credit card when you really need it, and don’t apply for credit cards in quick succession. That way getting new credit will be a neutral action that doesn’t set you back.

The type of credit and number of accounts you have also has an impact on your ability to win the game. If you pick up a diverse variety of debts along the way like a mortgage and other loans along with a credit card or two, you’ll have an easier time reaching your goal.

We have a few tips that can help put the big win within reach. Be aware that you can be penalized paying late as well as for moves that you didn’t actually take. This happens when negative items appear in your credit report by mistake – the credit bureaus think you made a bad move when you really didn’t. If this occurs, you have the right to dispute the item to have it removed. If you’re successful with a dispute, you’ll move up the board.

Additionally, players often think asking for help will set them back from reaching a winning credit score. But using services like credit counseling if you’re having trouble can actually help you move forward faster instead of setting you back. Completing a debt management program helps you eliminate credit card debt and may aid in helping you build a positive payment history. It can also help you avoid major setbacks on the board like debt settlement and bankruptcy. So you can get the help you need and still reach your ultimate credit goal, allowing you to win at the game of good credit to improve your financial standing overall.

Make the move to Consolidated Credit and let us help you develop a winning strategy to help you eliminate debt so you can achieve your credit goals.

-

Now PlayingGame of Good Credit: Your Credit Score

-

Up NextHow to Read a Credit Report

-

How Long Will Negative Items Affect You?

-

Understanding Credit Inquiries

-

Repairing Your Credit for Free

Questions? Our financial coaches are here to help! Just click the button to ask your question and we’ll get back to you ASAP!