The current real estate market is a seller’s market. Home inventory is low, which means high competition for houses and even higher prices, giving sellers, rather than buyers, the upper hand. Getting an offer accepted can be extremely difficult, especially for a first-time homebuyer, but it’s not impossible! This guide can help you learn how to make an offer on a house to increase your chances of getting your offer accepted.

What do I need to make an offer on a home?

You’ve found your dream home and you’re ready to write an offer, but what exactly do you need? These three things can give you the best chance of having your offer accepted.

1. A good real estate agent to handle the paperwork

Retaining a good real estate agent is highly recommended. Whether this is your first time buying a home or your tenth, an agent who understands your needs, the local market, and the right strategy to purchase each property can pay off in the long run.

As a first-time homebuyer, a real estate agent is essential. They will help you do everything from finding the right home to fit your needs and budget to helping you put an offer on a house in a way that’s likely to be accepted.

The agent will handle all the paperwork to submit the formal offer contract to the seller. Keep in mind that a real estate property offer is a legally binding contract. You can ask your agent to go through the contract with you, so you understand exactly what it says and what you’re committing to.

It’s worth noting that in 99.9% of cases, the seller pays the buyer agent’s commission, meaning you get all the agent’s knowledge and expertise for free.

2. A mortgage pre-approval letter to show you can afford the property

Its recommended to be pre-approved for a mortgage before even looking at any properties. Pre-approval will determine how much home you can afford, and save you precious time during the house hunt. It’s the best way to show real estate agents and buyers that you’re serious, and in many cases, you will need a pre-approval letter just to view a home.

Preapproval letters are obtained through a mortgage lender. This documentation shows how large of a mortgage the lender will be willing to extend to you and shows sellers that you have the finances to purchase their home. Your agent will include your preapproval letter or proof of finances in your offer.

3. Earnest money to show you’re a serious homebuyer

Your offer will can include what’s known as an “escrow deposit” or earnest money deposit.

Earnest money indicates to the seller that you are serious about purchasing the property. The deposit is used to protect the seller if you decide to walk away from the deal in any way that isn’t specified in the contract. If you do, you forfeit that earnest money deposit.

However, you won’t forfeit your escrow deposit for things such as the home appraisal showing the home is not worth the asking price or if major issues are discovered during your home inspection. These are known as contingencies, which we’ll explain in more detail below.

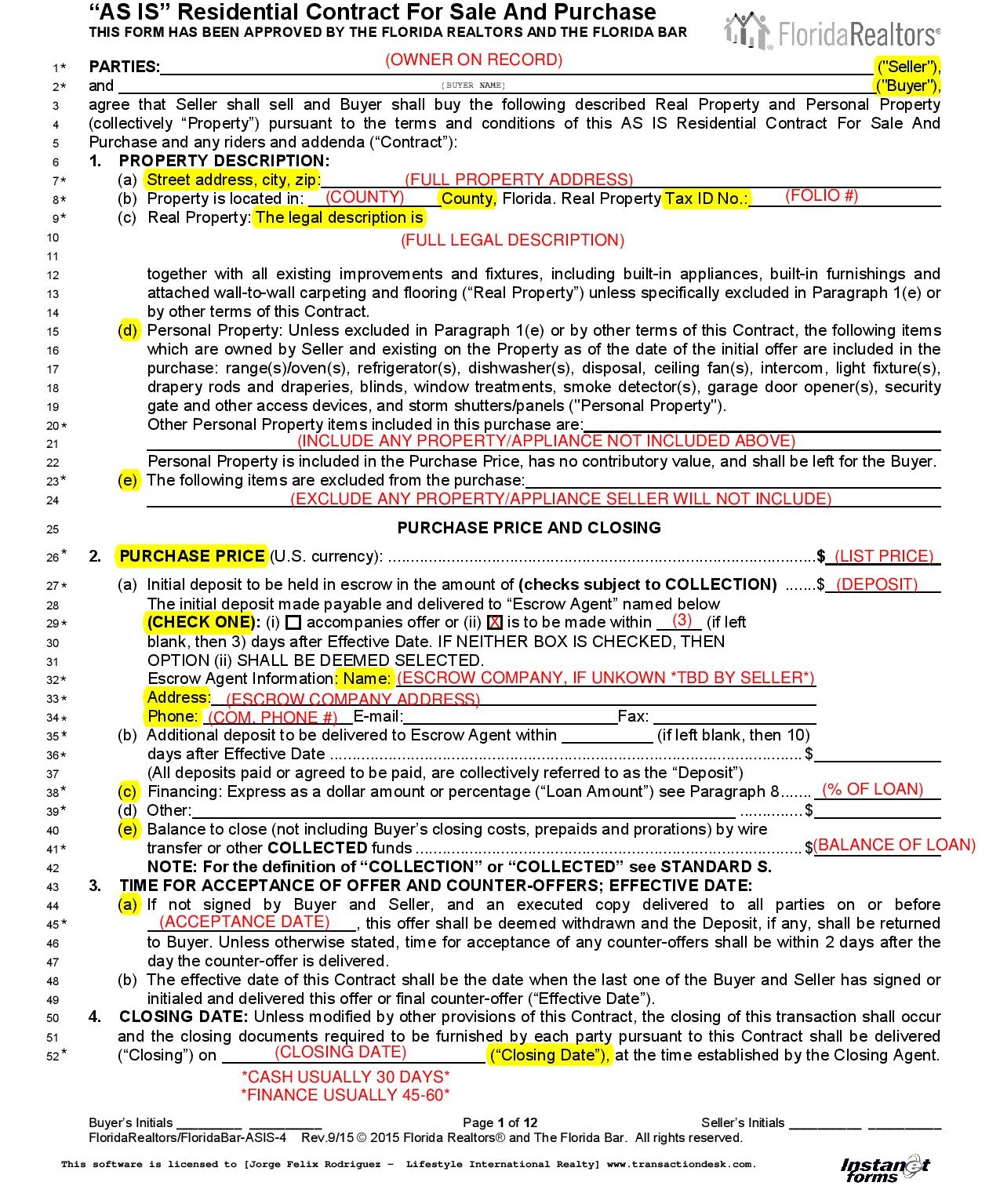

A sample offer contract in Florida

The below contract offers an example of a simple real estate purchase agreement used in Florida.

Determining your initial offer

You’ve crossed your T’s and dotted your I’s and are ready to submit an offer on a house. The seller is asking for $250,000 and you think that sounds reasonable, but how can you be sure? While deciding on the aspects of your initial offer, there are several key factors that you (and your agent) should take into consideration.

What are other homes selling for in the area?

This is a monetary estimate that considers a range of factors for the property you are trying to buy, to comparable homes in the surrounding area, including:

Age

Size

Construction

Style

Condition

A comparative market analysis can give you a clearer idea of why the price ranges in the area may differ.

How long has the property been on the market?

In cities where the market is hot, it usuallys takes less than 50 days for a home to sell. Houses that sit longer than this generally sell for less than the original asking price. Several factors can contribute to this, such as:

High HOA fees

High mandatory membership fees to live in a certain community

High cost of necessary repairs to the home

It can even be due to the seller’s situation, such as a seller who’s waiting for the highest and best offer with no rushed inclination to sell.

Other key details your offer needs to include

Aside from the offer price, there are some other key details that your offer will include:

Projected loan closing date

Mandate that the seller will provide clear title to the property (No liens from third parties that could pose a question to ownership)

State-required provisions or disclosures

Details regarding the buyer’s responsibility for closing costs or other fees, and how taxes and expenses are prorated between the buyer and seller

By the time you’re ready to make an offer, you should have a good idea of what the home is worth and what you can afford to pay. Be prepared for give-and-take negotiation once you’ve made the initial offer since it’s common for this to occur when buying a home. The buyer and seller often go back and forth until they can agree on a price and contingencies.

With that in mind, be prepared to receive counteroffers which you can discuss with your real estate agent.

Contingencies

While writing the offer contract, you and your agent will go over certain escape clauses, or contingencies, that allow you to walk away from the sale without losing your escrow deposit. The most common types of contingencies are the home inspection, appraisal, financing, and title. As you go through the process, called active approval, your offer will generally be contingent on 5 things:

Having financing at an interest rate not exceeding your budget

Home inspection did not reveal any significant issues with the home

Fully transparency from the seller to disclose any known issues

No major pest infestations or damage to the property

Seller completing an agreed upon repairs

These are a checks-and-balances system from the banks required by lenders to avoid lending any prospective buyer more than a home is worth.

Tips for putting an offer on a house

Be proactive: Don’t wait. If you see a home you like, make an offer promptly. Homes move very quickly in a seller’s market and by the time you make a final decision the house could be gone.

It will take time: It’s not uncommon to make offers on multiple properties before finally getting a ‘yes’. Be patient. Getting caught in a bidding war will have you spending more money than the house is worth or more than you’re comfortable spending (which is always a mistake).

Don’t make rash decisions: Buying a home you’re not fully invested in just because you’re tired of missing out can be a grave mistake. Remember, buying a home is often a 30-year commitment. Take your time, reassess your options and make an offer based on logic rather than emotions.

Finally, keep in mind that making an offer on a home is just one step in the process.