The credit score impact of medical debt collections

The Consumer Financial Protection Bureau (CFPB) recently announced a rule barring medical debt from appearing on credit reports (effective 60 days from January 7, 2025). This rule will significantly altered the financial landscape for many Americans.

While this is a major step towards reducing the burden of medical debt, it’s crucial to understand that non-payment of medical bills still has consequences. Debts can still be sent to collections, and you may face legal actions for non-payment.

Avoiding collections

Even without the credit reporting impact, hospitals and doctors’ offices will still pursue payment. This may involve repeated calls and letters. So, you want to avoid having an account fall into collections if possible. This means being proactive when it comes to covering these expenses. If you have bills already or you are getting a procedure or treatment that your insurance won’t cover, consider your options immediately. You can:

- Talk to the service provider about setting up a payment plan for the bill. Some providers even offer income-based plans if you are living paycheck-to-paycheck or facing financial hardship as a result of your debt.

- Consider getting a personal loan to pay your medical bills. You can ask the provider for a cost estimate of all the procedures, treatments, and prescriptions that you need that aren’t covered by insurance, then take out an amount that will cover it.

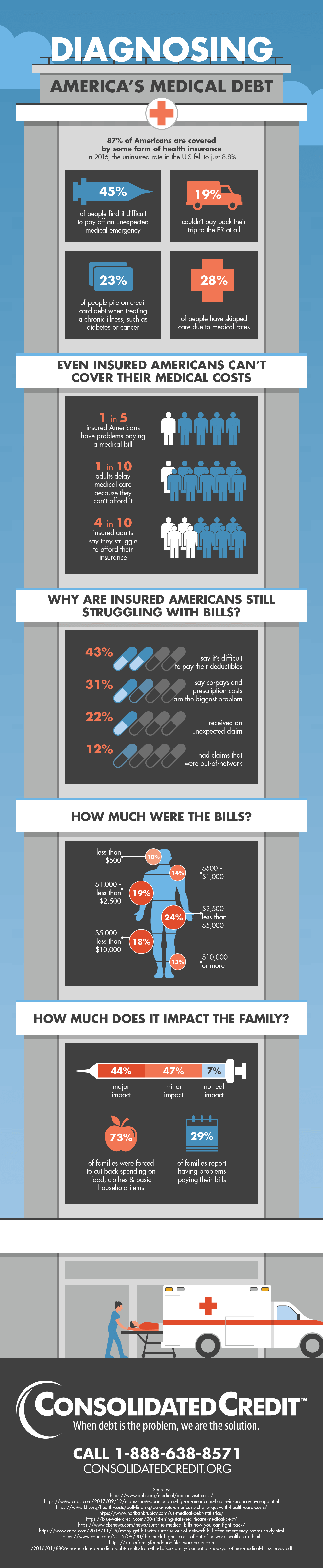

- See about getting a medical credit card. There are credit cards specifically meant to cover medical expenses. Just be aware that you’re likely to pay a much higher interest rate if you do not pay off the balance promptly.

- Weigh the risks and benefits of borrowing against home equity. If you are a homeowner and your income is steady and won’t be affected by your medical issues, then you may want to consider options to borrow against the equity you have in your home. Just be aware that this may increase your risk of foreclosure, so you want to make sure you can keep up with the payments.

How to get out of medical debt

If you have unpaid medical bills that turned into collection accounts, here is what you need to know about the best ways to eliminate the debt.

Can I use debt consolidation?

Yes. There are several ways that you can consolidate these debts with other unsecured debts that you need to pay:

- Use funds from a debt consolidation loan to pay off unpaid medical bills. If you take out a personal debt consolidation loan, you can ask the lender to disburse a portion of the funds you receive to pay off medical debt collectors. This is a type of do-it-yourself debt consolidation.

- You may be able to include unpaid medical bills in a debt management program. If you sign up for a debt management program, you can request for unpaid medical bills to be included. The medical service provider or collection agency must approve the adjusted payment schedule. Otherwise, the debt cannot be included.

Is it in my best interest to consolidate medical debt?

It’s important to note that medical debt does not have any interest rate applied to it. Even if a medical bill passes to collections, it may accrue penalties but there is still no applied interest rate.

This means if you use a debt consolidation loan to get out of medical debt, you convert debt with no interest charges to debt that has interest charges applied. Although it gives you the means to eliminate the collections account, it also means the debt will cost more to pay off. In other words, the total cost of eliminating the debt increases.

With a debt management program, the credit counseling agency calls each of your creditors to negotiate. The goal is to reduce or eliminate interest charges applied to your debt. So including medical debt in the program won’t add interest charges. However, you don’t benefit from the credit counseling agency being able to negotiate on your behalf.

For that reason, a debt management program is not typically used to consolidate medical debt only. You’re missing out on one of the main benefits. People typically only use a debt management program to consolidate medical debt when they have other bills to consolidate, too. If you have a combination of credit cards and other unsecured debts along with medical debt, then it makes sense.

Learn more about consolidating debts in collections »

If I don’t consolidate, what can I do?

First, make sure to request a copy of the claim and review it carefully. Medical bills may include charges for procedures you never received. Keep that in mind and make sure the bill is accurate for the medical services you received. If you have several bills and you have questions over their accuracy, you can hire an auditor. They review the bills and work to reduce the amount you owe.

Next, call the original medical service provider. They may be willing to set up a payment plan or accept a settlement offer. A payment plan splits the total bill up into installments you pay over a period of months. A settlement eliminates the debt for less than the full amount owed.

If the original provider won’t accept payment directly, you can work with the collector. Again you want to request either a settlement or payment plan. Be aware that any debt paid for less than the full amount owed also results in negative credit information.