The first of the year is always a time for setting goals. But if you really want to get ahead, you need to know exactly where you’re starting out and where you want to go. It’s the only way to reach your destination effectively, with as little time and effort wasted as possible.

If you’re looking to improve your financial outlook in 2014, you’re not alone. Improving financial health is now the second most popular New Year’s resolution after dieting. Unfortunately, like most resolutions, simply making a goal is never enough.

With that in mind, Consolidated Credit has identified five important indicators of financial health that you can use as mile markers on your road to financial success. If you pay attention to these five factors this year and work to improve your standing in each, you can be guaranteed to get ahead financially this year.

Here are some steps you can take to get ahead with each of these five factors:

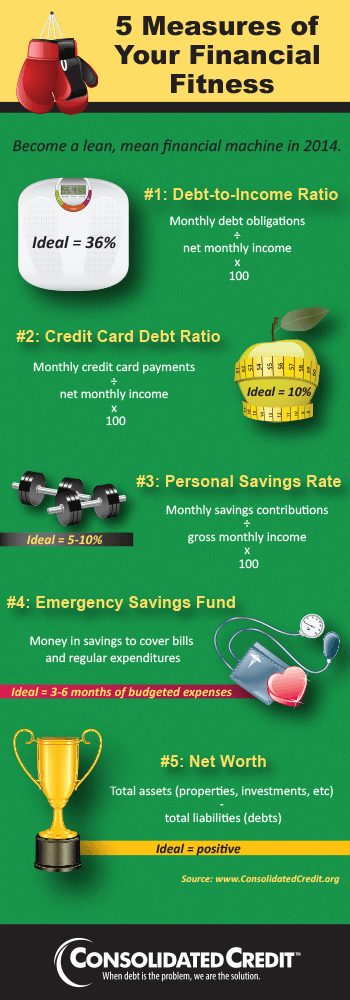

No. 1: Debt-to-Income Ratio

This leading indicator of your financial health measure how much debt you pay off each month versus how much money you bring home in your paychecks. The easiest ways to improve your debt-to-income ratio are to take steps to pay off credit card debt (see below) or consider downsizing, by selling off assets like cars or a property that’s more home than you can afford.

No. 2: Credit Card Debt Ratio

It may sound odd, but the way to improve the amount of income you devote to credit card debt payments is to make a plan to put as much income as possible towards eliminating credit card debt. The more debt you pay off quickly, the lower your bills will be in the coming months.

No. 3: Personal Savings Rate

Every month you need to pay yourself, just like you pay your creditors and lenders. Leaving savings as an afterthought if you have money left at the end of the month is a good way to ensure you never save anything at all.

Determine how much money you have available in your budget and make this a monthly “obligation” that you pay to yourself. You can even set up a recurring account transfer to move the money from checking to savings by a certain date so saving money is automatic every month.

No. 4: Emergency Savings Fund

Emergency savings allows you to get past financial speed bumps without letting them slow you down. Essentially, it gives you money to cover all your bills and regular monthly expenses like groceries. This way, if an income earner loses their job or has their hours cut, you can stay ahead without relying on credit cards.

No. 5: Net Worth

Positive net worth means financial stability. It means that even if you get into trouble and drain your emergency savings completely, you could still stay ahead with your assets. If you’ve done everything else for your finances on the list, then look to build wealth.