Identity Theft Resources

Learn how to prevent ID theft and handle it quickly if it happens to you.

Identity theft remains one of the most widespread and damaging crimes in the U.S. In 2024 alone, the federal government’s consumer complaint portal received more than 1.1 million identity-theft reports and related fraud complaints pushed the estimated losses nationwide above $12.7 billion.

More recent consumer survey data suggest that victims are more common than many realize. According to Debt.com’s 2025 identity-theft survey of 1,000 U.S. adults, 78% said they had been victimized at some point, a dramatic increase from 43% in the prior survey, reflecting a sharp rise in reported ID-theft experiences nationwide.

Because identity theft is pervasive and evolving – with growing threats from AI-enabled scams, fraud targeting children, and credit-score damage – it’s more important than ever to know how to protect yourself and recover quickly if you become a victim. This resource center helps you learn what ID theft looks like, how to guard your personal information, and what to do if your identity is stolen.

What the latest data shows

Debt.com’s 2025 survey revealed several troubling trends:

- A dramatic rise in victimization: 78% of respondents reported that they had experienced identity theft, up from 43% just a year earlier.

- Growing impact on families: 61% said a child or family member had their identity compromised, highlighting rising risk among youth, too.

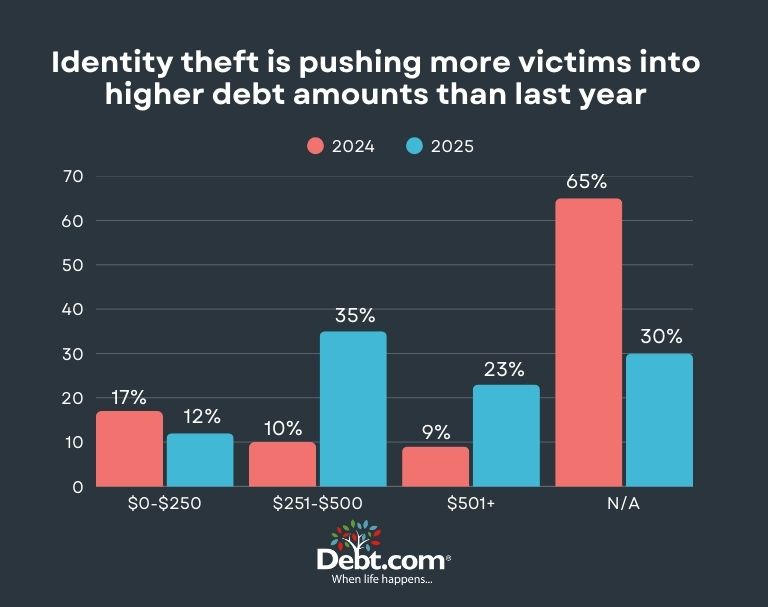

- Financial consequences are substantial: 57% of victims said ID theft forced them into debt, and many lost hundreds or thousands of dollars trying to reclaim their identity or correct their credit.

- Credit score damage is common: A significant portion of victims reported credit score drops, including 21–50 point drops and, in many cases, even larger declines.

- New scams are fueling the surge: Nearly 90% of surveyed adults predicted that AI-powered fraud will contribute to increased ID theft in the near future.