New Consolidated Credit Survey: One in Five Americans Wait Until a “Last Resort” to Address Record-High Credit Card Debt

June 2, 2026

While 70% of consumers trust nonprofit credit counseling, nearly half are unaware of the most effective solution for the $1.3 trillion national debt crisis: The Debt Management Program.

Read full article

Consolidated Credit Recognizes Community Partners at 12th Annual National Financial Literacy Month Breakfast

April 9, 2026

Consolidated Credit celebrates Financial Literacy Month with community partners.

Read full article

Consolidated Credit Offers Free Webinar Series Focused on Caring for Your Mental and Financial Health, Saving Strategies for Summer Vacation, and New Rules for Student Debt

April 1, 2026

Free monthly webinars offer practical tools to help consumers reduce money stress and anxiety, save smarter for summertime fun, and navigate the latest policy on student loan debt.

Read full article

Consolidated Credit Renews Partnership with Junior Achievement to Expand Financial Education

February 5, 2026

Hands-on financial education will reach tens of thousands of students through JA World programs and storefront learning experiences.

Read full article

Consolidated Credit Starts Off the New Year with New Webinar Series Focused on the Best Debt Strategy, Preparing for Tax Season, and Earning Financial Freedom

January 15, 2026

New Year, new webinar series focused on best debt strategy, preparing for tax season, and earning financial freedom.

Read full article

Consolidated Credit Proudly Supports the 2025 Joe DiMaggio Red Gala Fundraiser

November 19, 2025

Consolidated Credit proudly supports Joe DiMaggio Children's Hospital Foundation, making a difference in the lives of children and families.

Read full article

Consolidated Credit Survey: Americans Still Carrying Last Year’s Holiday Debt — and It’s Shaping 2025 Decisions

November 6, 2025

Past holiday debt shaping the way consumers spend on 2025 holidays.

Read full article

Community Outreach Manager Leads Workshop for MOMS Program Through Memorial Healthcare System

October 30, 2025

Press Releases from Consolidated Credit - Community Outreach Manager Leads Workshop for MOMS Program

Read full article

Consolidated Credit Partners with Community-Based Foundation

October 23, 2025

Consolidated Credit collaborates with foundation to introduce high school seniors to entrepreneurship.

Read full article

Consolidated Credit Attends University of Miami’s Entrepreneur Business-Building Event

October 17, 2025

University of Miami business-building event brings together entrepreneurs, speakers and exhibitors to share knowledge, tools, and purpose.

Read full article

Consolidated Credit Attends PNC Small Business Collaboration Event

October 16, 2025

PNC Bank community partners and Consolidated Credit celebrate Hispanic heritage at luncheon.

Read full article

Consolidated Credit Joins Hispanic Entrepreneurs Initiative Celebrating Proclamation

October 1, 2025

Hispanic entrepreneurs celebrate proclamation honoring their achievements and contributions to the community.

Read full article

Consolidated Credit And SCORE Broward Hold Panel Discussion Focused On Spanish-Speaking Small Business Owners and Startups

September 20, 2025

Attendees receive valuable education about first steps to small business ownership.

Read full article

Consolidated Credit and Community Partner LifeNet4Families Educate On Identity Theft

September 18, 2025

Press Releases from Consolidated Credit - Consolidated Credit and Community Partner LifeNet4Families Educate On Identity Theft

Read full article

Consolidated Credit Proudly Joins as Partner Resource for United Way of Broward Conversemos entre Mujeres

August 22, 2025

Consolidated Credit provides vital financial information to help families in the community.

Read full article

Consolidated Credit Participates in Broward Partnership Housing Resource Fair

August 14, 2025

Consolidated Credit offers financial education and resources for housing fair.

Read full article

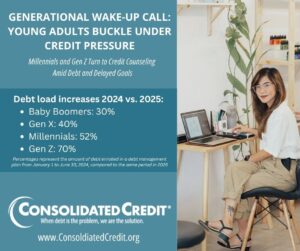

Generational Wake-Up Call: Young Adults Buckle Under Credit Pressure

August 12, 2025

As Millennials and Gen Z face soaring interest rates, record balances, and delayed financial milestones, Consolidated Credit finds demand for counseling spikes.

Read full article

Summer Spending Spree: How to Avoid Financial Pitfalls During Peak Season

July 30, 2025

From cooling costs to summer vacations and back-to-school shopping, the season often brings a surge in consumer spending that can lead to financial stress if left unchecked.

Read full article

Consolidated Credit and the Hispanic Heritage Chamber of Commerce Collaborate to Strengthen Growth of Hispanic Business Community

July 18, 2025

Consolidated Credit and the Hispanic Heritage Chamber of Commerce committed to growth and stability of Hispanic businesses and entrepreneurs.

Read full article

Consolidated Credit and Community Partner LifeNet4Families Host Final Workshop in Series

July 17, 2025

Press Releases from Consolidated Credit - Consolidated Credit and Community Partner LifeNet4Families Host Final Workshop

Read full article

Consolidated Credit Showcases Wide Range of Services and Highlights Service to the Community at the Broward Affordable Housing Task Force Meeting

June 25, 2025

Director of Housing Counseling and Community Outreach highlights the wide array of services available to the community, and our commitment to serving the Broward community.

Read full article