Find out how Consolidated Credit can help you!

Michigan Debt Relief Guide

The outlook for “The Great Lakes State” is good. Both production and demand for manufactured goods are on the rise. Michigan ranks 14th in economy size in the United States, and many industries, including retail trade, information, and construction, are experiencing promising GDP growth.

However, many residents who held lower-wage and lower-skilled jobs are still unemployed, and inflation is also hurting them.

“The situation is challenging for Michiganders,” says Gary Herman, President of Consolidated Credit, “The state’s service sectors are still suffering. Pair that with the inflation we’re seeing nationwide, and it’s a recipe for credit card debt.”

The latest available data says that the average Michigan household has $9,493 in credit card debt. Citizens in this state collectively owe $34,713,007,245, an increase of $968,790,521 from the beginning of the year

If you’re curious how we can help you, below you will find a few case studies from clients we’ve helped in Michigan residents. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

Consolidated Credit Helps Michigan Residents Reduce Their Total Credit Card Payments by Up to 50%

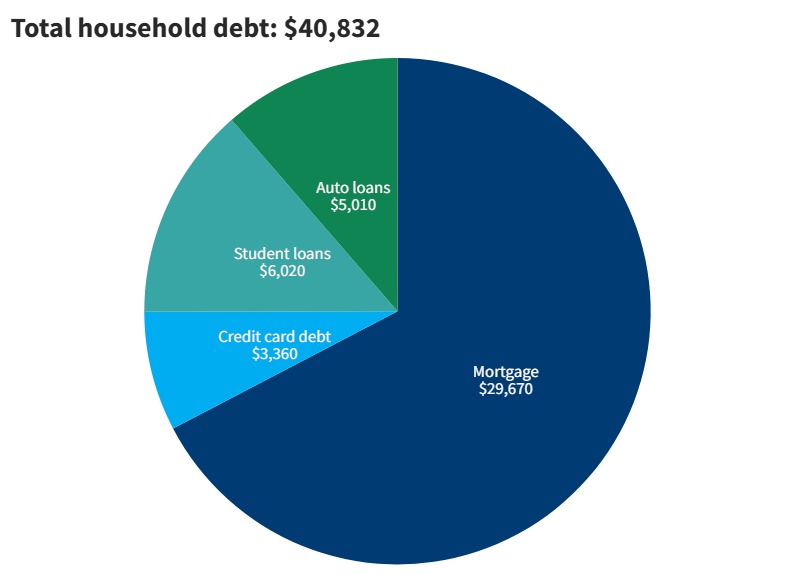

Consumer debt in Michigan

This chart shows a breakdown of average consumer debt in Michigan based on the latest Household Debt report from the Federal Reserve.

In 2024, 13,899 Michigan residents filed for bankruptcy.

Income and employment in Michigan

Regarding pay, Michigan has an average per capita income of $37,929 and a median household income of $68,505. The minimum wage increased to $12.48 per hour after the state supreme court decision in 2024.

Michigan is a right-to-work state, which means workers are not required to join a union or pay membership dues; however, they can join unions if they choose.

Michigan is also one of the top five states for FDI (Foreign Direct Investments). Global companies have invested nearly $12 billion in Michigan, creating over 36,000 jobs.

This demand for workers is good for Michigan residents. New employment opportunities can help individuals and families improve their financial situation.

If you are unemployed in Michigan, your unemployment insurance will last 26 weeks.

Apply for unemployment benefits in Michigan »

Banking and taxes in Michigan

Michigan residents pay a low, flat-rate state income tax of 4.25%, which makes their finances a little easier, and a sales tax of 6%. Unlike many states, Michigan does not have a tax-free holiday or weekend.

Michigan residents are also less likely to bank than the average American. The percentage of unbanked residents without a checking or savings account stands at 5.7%, just above the national average of 5.1%.

Michigan housing market

With an average house price of just $245,716, homeownership in Michigan is far more affordable than in many other states. Listings still get top dollar, but the market is cooling down.

- 74.1% of Michigan residents are homeowners

- Median monthly owner cost, including mortgage: $1,472

- Median rent payment: $1,037

Michigan has help for renters who are having difficulty making their rent payments. Homeowners in Michigan can also get help with their mortgage payments, and an online portal is currently under development.

Talk to a HUD-certified housing counselor to get help with the housing challenges you’re facing.

Retirement in Michigan

US News and World Report ranked six Michigan cities among the 150 best for retirees. Ann Arbor, home to the University of Michigan, was ninth.

CNBC reported in 2024 that the average Michigan resident would need about $53,121 annually to retire. A 20% comfort buffer ($10,624) is recommended. That means the target for a comfortable retirement in Michigan would be about $63,745.

Michigan offers low living costs and a low poverty rate for seniors, making retirement there a good choice. Michigan is also tax-friendly, with no Social Security tax and only partially taxed pensions and withdrawals from retirement accounts.

Average Michigan insurance premiums

Michigan residents enjoy mostly lower-than-average rates for protecting their homes, vehicles, and health with insurance.

Homeowners insurance rates are slightly lower than the national average of $2,304. The average Michigan homeowner’s insurance premium is $2,040.

The average cost of health insurance in Michigan is $6,800, and the average cost for annual auto insurance is $3,049.

Helpful resources for Michigan residents facing hardship

Food insecurity

| Region | Food Bank | Phone Number | Address |

|---|---|---|---|

| Central Michigan | Mason Food Bank | (517) 676-2563 | 118 W. Oak Street Mason, MI 48854 |

| Central Michigan | Food Bank Council of Michigan | (517) 485-1202 | 330 Marshall Street Suite 103 Lansing, MI 48912 |

| Central Michigan | Food Bank of Eastern Michigan | (810) 239-4441 | 2300 Lapeer Road Flint, Michigan 48503 |

| Central Michigan | Holt Community Food Bank | (517) 694-9307 | 2021 Aurelius Road PO Box 577, Holt, MI 48842 |

| Central Michigan | Greater Lansing Food Bank | (517) 853-7800 | 5600 Food Court Bath, MI 48808 |

| Central Michigan | Roscommon County Food Pantry | (989) 202-4889 | 725 S Loxley Rd Houghton Lake, MI, MI 48629 |

| Metro Detroit | Gleaners Community Food Bank of Southeastern Michigan | (866) 453-2637 | 2131 Beaufait Detroit, MI 48207 |

| Metro Detroit | Nourishing Gardens Food Bank | (734) 713-7715 | 24831 Sumpter Road Belleville, MI 48111 |

| Metro Detroit | Joan & Wayne Webber Distribution | (586) 758-6815 | 24162 Mound Rd Warren, MI 48091 |

| Metro Detroit | Bountiful Harvest | (810) 360-0271 | 290 E Grand River Rd, Brighton, MI 48116 |

| Southern Michigan | South Michigan Food Bank | 269-964-3663 | 5451 Wayne Rd Battle Creek, MI 49037 |

| Southern Michigan | Brooklyn Food Pantry | (517) 612-8771 | 171 Wamplers Lake Rd, Brooklyn, MI 49230 |

| South-Central Michigan | Branch Area Food Pantry | (517) 279-0966 | 22 Pierson St. Coldwater, MI 49036 |

| South-Central Michigan | Jackson Community Food Pantry | (517) 962-1005 | 701 Greenwood St. Jackson, MI 49203 |

| South-East Michigan | Open Hands Food Pantry | (248) 546-1255 | St. John’s Episcopal Church 26998 Woodward Avenue at 11 Mile Royal Oak MI 48067 |

| South-East Michigan | Neighborhood House Food Pantry | (248) 656-4904 | 1720 South Livernois Road Rochester Hills, MI, 48307 United States |

| West-Central Michigan | Feeding America West Michigan | (616) 784-3250 | 864 West River Center Drive NE, Comstock Park, MI 49321 |

Veterans

According to the Census Bureau, Michigan is home to 498,788 veterans. These resources are available to help veterans facing unemployment, homelessness, and other hardships.

Veteran Resources:

National crisis hotline: (800) 273-8255

Department of Veterans Services

Michigan Veterans Affairs Agency

3423 N. Martin Luther King Jr. Blvd.

Bldg 32

Lansing, MI 48906

800-MICH-VET (800-642-4838)

MVAAResourceCenter@michigan.gov

Find a Veteran service office in your area »

Helpful employment resources for Veterans:

- CareerOneStop

- VeteranRecruiting.com

- Helmets to Hardhats

- Hiring Our Heroes

- My Next Move

- Warriors to Work

How Consolidated Credit helps Michigan residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 4,539 Michigan residents. Of those, 854 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $12,819). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution to get out of debt as quickly as possible.

We’d also like to congratulate the 300 Michigan residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Michigan

A debt consolidation loan is an unsecured personal loan that you get to pay off credit cards and other existing debts. You need good credit to qualify for the lowest interest rate possible. That low rate helps lower your total payments so you can get out of debt faster, even though you may pay less each month. So, this is a good solution for Michigan residents with a high credit score.

A home equity loan or home equity loan of credit (HELOC) is a debt solution that’s only available to Michigan homeowners. If you have equity available in your home, you can borrow against that equity and use the funds to pay off your debt. However, this can be a risky option for paying off credit card debt if you are living paycheck-to-paycheck. Home equity lending products put consumers at risk of foreclosure if they can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Nonprofit credit counseling services like those provided by Consolidated Credit help consumers identify the best solution for getting out of debt. This is a free service. Michigan residents can get a confidential debt and budget evaluation from a certified credit counselor. Then the counselor will explain options that are available to each person and recommend the best course of action based on an individual’s needs and goals.

If a Michigan consumer cannot get out of debt effectively on their own but has the ability to repay everything they owe to avoid bankruptcy, a debt management program is often the best solution. You enroll in the program through a credit counseling organization. They help you find a monthly payment you can afford and then work with your creditors to reduce or eliminate interest. Qualifying residents can get out of debt in 36-60 payments.

Debt settlement allows Michigan residents to get out of debt for a percentage of what they owe. You can settle debt on your own and negotiate with individual creditors and collectors or enroll in a debt settlement program to get professional help. This does cause credit damage. Each debt settled will be noted on your credit report for seven years from the date the account first became delinquent. However, it can be a viable debt relief option for avoiding bankruptcy when you are completely overwhelmed with debt.

Ready to see if Consolidated Credit can help you, too? Talk to a certified credit counselor for a free debt and budget evaluation.

Want to know if Consolidated Credit can help you, too? Get a free, confidential debt and budget analysis now.