Find out how Consolidated Credit can help you!

North Carolina Debt Relief Guide

The “Tar Heel” state has suffered and grown over the past few years.

A long-term decline in local manufacturing has hit small towns and communities particularly hard. Meanwhile, larger cities have done very well, fueled by a boom in financial and technology industries.

However, the state has a great deal of poverty and long-term unemployment.

“The story for North Carolina technology and banking workers is great. But households in the manufacturing and agriculture sectors are struggling,” Gary Herman, President of Consolidated Credit, stated. “People and families who are facing challenges like reduced income or unemployment must focus on paying down debt and increasing their savings. That way, they can achieve and maintain financial stability even in the face of potential economic challenges down the road.”

The latest available data says that the average North Carolina household has $10,412 in credit card debt. Citizens in this state collectively owe $38,984,626,014, an increase of $1,088,005,308 from the beginning of the year.

How Much Could You Save?

Just tell us how much you owe, in total, and we’ll estimate your new consolidated monthly payment.

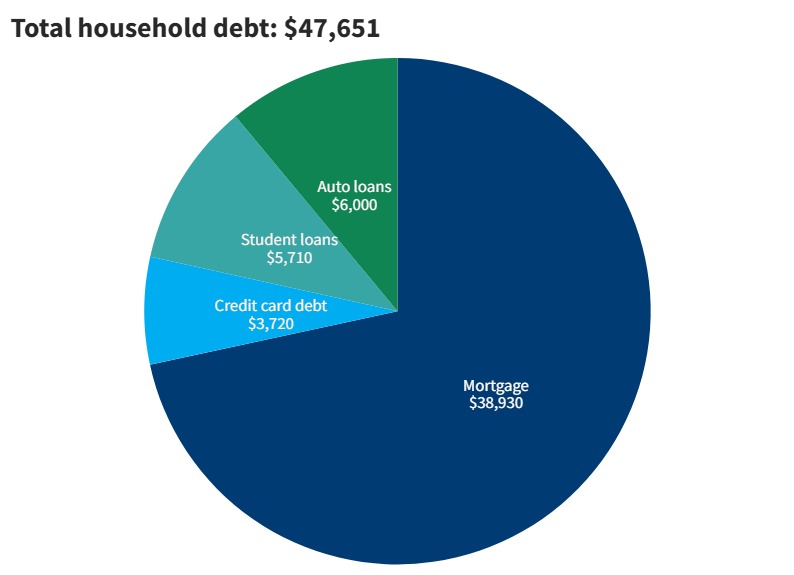

Consumer debt in North Carolina

This chart shows a breakdown of average consumer debt in North Carolina, based on the latest report of Household Debt report from the Federal Reserve.

According to the latest data available, in 2023, there were 7,452 bankruptcy filings in North Carolina.

Income and employment in North Carolina

North Carolina continues to be an economically divided state. While metropolitan areas are growing, rural communities have been particularly hard hit.

North Carolina continues to be an economically divided state. While metropolitan areas are growing, rural communities have been particularly hard hit.

Agriculture is still a dominant industry in North Carolina. The industry supports nearly 700,000 jobs.

At the same time, Charlotte and other larger cities are growing. Charlotte is the sixteenth largest city in the U.S. and is the second-largest banking center after New York.

North Carolina is a right-to-work state. That means workers are not required to pay union membership dues even if they are at their workplace, but they can still choose to do so.

North Carolina’s pay rates could be better. The state has a per capita income of $37,641 and a median household income of $66,186. The minimum wage is $7.25 per hour.

If you are unemployed in North Carolina, your Unemployment Insurance will last 12 weeks.

Apply for unemployment benefits in North Carolina»

To file a claim by telephone number: 1-888-737-0259

Banking and taxes in North Carolina

North Carolina residents pay a state income tax of 4.5% and a sales tax of 4.75%. The state doesn’t have any tax-free holidays.

North Carolina residents are slightly more likely to bank than the average American. The percentage of unbanked residents — those without a checking or savings account stands at 5.4%. That’s marginally lower than the national average of 6%.

North Carolina housing market

In recent years, Raleigh and Charlotte made Zillow’s top 10 list of hottest real estate markets. While the market is expected to slow somewhat, the seller’s market remains. The average price for a home in North Carolina is $329,341, slightly lower than the national average of $408,800. Despite relatively low pricing in the state, there is still an affordability crisis. Many younger buyers and lower-income earners are getting priced out of the market.

North Carolina residents can take advantage of homestead deductions. There are also deductions for residents above the age of 65, for those who are permanently or totally disabled, and for historic properties.

Don’t keep struggling on your own to eliminate your high interest rate credit card debt. Talk to a certified credit counselor to find the right debt relief option for your situation.

Retirement in North Carolina

For retirees, taxes in North Carolina can be good. Social Security income is not taxed, but income from retirement accounts such as 401(k) pensions is taxed at the state income tax of 4.5%. Overall, there is a lower-than-average cost of living. However, the crime rate is slightly higher than average.

The Charlotte Observer reported that residents need an average of $69,237 a month to retire comfortably in North Carolina. The average resident retires at age 63. About 25% of retirees rely upon Social Security for at least 90% of their income.

Average North Carolina insurance premiums

In North Carolina, car insurance rates depend partly on your credit score. For example, those with a poor credit score can expect to pay $2,858 on their annual premium. In comparison, those with an excellent credit score will play closer to $1,985.

The average amount North Carolinians pay for homeowner’s insurance is $2,435 per year, which is higher than the national average of $1,754.

Health insurance in North Carolina averages around $6,352. However, the state has the 10th highest uninsured rate in the United States.

Helpful resources for North Carolina residents facing hardship

Food insecurity

| Region | Food Bank | Phone Number | Address |

|---|---|---|---|

| Atlantic coastal plain region | Second Harvest Food Bank of Northwest North Carolina | (336) 784-5770 | 3655 Reed St. Winston-Salem, NC 27107 |

| Atlantic coastal plain region | Holly Springs Food Cupboard | (919) 577-2210 | 621 W Holly Springs Road | PO Box 268 | Holly Springs, NC 27540 |

| Atlantic coastal plain region | Samaritan’s Shelf Food Pantry | (919) 553-4332 | 143 Short Johnson Rd, Clayton, NC 27520 |

| Atlantic coastal plain region | Fuquay Varina Emergency Food Pantry | (919) 552-7720 | 216 West Academy Street Fuquay Varina, NC 27526 |

| Southeastern North Carolina | Food Bank CENC at Wilmington | (910) 251-1465 | 1314 Marstellar Street, Wilmington, NC 28401 |

| Southeastern North Carolina | WEUMC Food Pantry | (910) 673-1371 | 4015 Highway 73, West End, NC 27376 |

| Southeastern North Carolina | Mother Hubbard’s Cupboard | (910) 762-2199 | 315 Red Cross Street Wilmington, NC 28401 |

| Southeastern North Carolina | Second Harvest Food Bank of Southeast North Carolina (SHFB) | (910) 485-6923 | 406 Deep Creek Rd Fayetteville, NC 28312 |

| Southeastern North Carolina | Christian Community Caring Center | (910) 270-0930 | 15200 US Hwy 17 Hampstead, NC 28443 |

| Piedmont | Hearts and Hands Food Pantry | (980) 292-0357 | 202 South Old Statesville Road Huntersville, NC 28078 |

| Piedmont | Beloved Street Pantry | (828) 571-0766 | 1302 Patton Ave. # 6386 Asheville, NC 28806 |

| Research Triangle | Inter-Faith Food Shuttle | (919) 250-0043 | 1001 BLAIR DRIVE, SUITE 120, RALEIGH, NC 27603 |

| Research Triangle | Tri-Area Ministry Food Pantry | (919) 556-7144 | 149 E Holding Avenue Wake Forest, NC 27587 |

| Research Triangle | Food Bank of Central & Eastern North Carolina | (919) 875-0707 | 1924 Capital Boulevard, Raleigh, NC 27604 |

Veterans

North Carolina is home to 720,000 veterans. These resources are available to help Veterans that are facing unemployment, homelessness, and other hardships.

Veteran Resources:

North Carolina Department of Veterans Services

413 North Salisbury Street

Raleigh, NC& 27603

844-624-8387

Find Veterans’ services in your area »

National crisis hotline: (800) 273-8255

Helpful employment resources for Veterans:

How Consolidated Credit helps North Carolina residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 5,534 North Carolina residents. Of those, 1,076 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $12,762). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution for their situation to get out of debt as quickly as possible.

We’d also like to congratulate the 409 North Carolina residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in North Carolina

A debt consolidation loan is an unsecured personal loan that you get to pay off credit cards and other existing debts. You need good credit to qualify for the lowest interest rate possible. That low rate helps lower your total payments so you can get out of debt faster, even though you may pay less each month. So, this is a good solution for North Carolina residents with a high credit score.

A home equity loan or home equity loan of credit (HELOC) is a debt solution that’s only available to North Carolina homeowners. If you have equity available in your home, you can borrow against that equity and use the funds to pay off your debt. However, this can be a risky option for paying off credit card debt if you are living paycheck-to-paycheck. Home equity lending products put consumers at risk of foreclosure if they can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Nonprofit credit counseling services like those provided by Consolidated Credit help consumers identify the best solution for getting out of debt. This is a free service. North Carolina residents can get a confidential debt and budget evaluation from a certified credit counselor. Then the counselor will explain options that are available to each person and recommend the best course of action based on an individual’s needs and goals.

If a North Carolina consumer cannot get out of debt effectively on their own but has the ability to repay everything they owe to avoid bankruptcy, a debt management program is often the best solution. You enroll in the program through a credit counseling organization. They help you find a monthly payment you can afford and then work with your creditors to reduce or eliminate interest. Qualifying residents can get out of debt in 36-60 payments.

Debt settlement allows North Carolina residents to get out of debt for a percentage of what they owe. You can settle debt on your own and negotiate with individual creditors and collectors or enroll in a debt settlement program to get professional help. This does cause credit damage. Each debt settled will be noted on your credit report for seven years from the date the account first became delinquent. However, it can be a viable debt relief option for avoiding bankruptcy when you are completely overwhelmed with debt

If you’re curious how we can help you, below you will find a few case studies from clients that we’ve helped in North Carolina. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

Ready to solve your problems with debt? Talk to a certified credit counselor for free to find the best way to get out of debt for you.