One of the most unique states in the country, Wisconsin is home to “cheeseheads” (fans of the Green Bay Packers and cheese fanatics alike). For years, the “Badger State” has drawn people in with its low cost of living and low housing prices.

The latest available data says that the average Wisconsin household has $8,357 in credit card debt. Citizens in this state collectively owe $18,488,234,969, an increase of $515,980,268 from the beginning of the year.

“Carrying credit card balances that high is not good for people’s budgets, especially when we’re already getting squeezed by inflation,” says Gary Herman, President of Consolidated Credit. “Paying off credit card debt as quickly as possible to eliminate those bills can be immensely beneficial right now. It will make it easier to maintain financial stability in the face of rising costs.

Consolidated Credit Helps Wisconsin Residents Reduce Their Total Credit Card Payments by Up to 50%

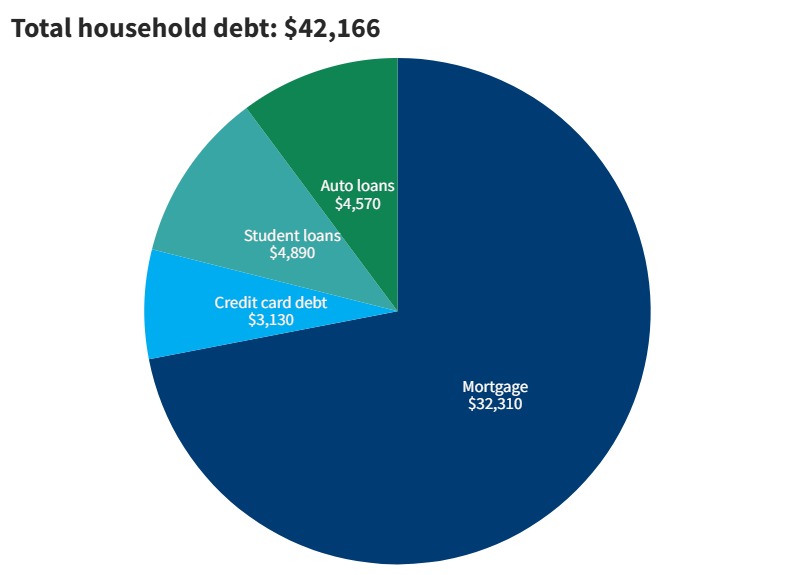

This chart shows a breakdown of average consumer debt in Wisconsin based on the latest Household Debt report from the Federal Reserve.

In 2023, 8,469 Wisconsinites filed for bankruptcy.

Income and employment in Wisconsin

Since Wisconsin is a right-to-work state, employees cannot be denied employment whether they are part of a union. Additionally, employees cannot be forced to join or leave a union against their will, nor are they obligated to pay union dues. Regardless of their union membership, employees can still enjoy the union benefits.

Furthermore, Wisconsin is an employment-at-will state. This means that an employer can terminate employment at any given moment and for any reason. Conversely, employees can also resign in a similar fashion. In layman’s terms, neither the employer nor the employee guarantees they will uphold employment.

As of September 2024, the unemployment rate in Wisconsin is 2.9%, 1.2 percentage points below the national unemployment rate of 4.1%.

Wisconsin has an individual income tax that ranges between 3.5% and 7.65%. The state also imposes a state sales tax of 5%. The total sales tax rate can range between 5%-5.5% when combined with local taxes.

Banking is fairly common in Wisconsin, as only 2% of residents have a checking or savings account.

Wisconsin housing market

As of 2024, Wisconsin is a seller’s market, where sellers have more leverage because the area is in high demand. That said, the housing market is not notably competitive compared to other states. Two important markers are down from 2023: a number of homes sold and the cost of homes.

Milwaukee, for example, is suffering from a lack of new construction due in part to decreasing labor forces, increasing interest rates, higher material prices, and unpredictable permitting processes. Most people look to Milwaukee for its low average home prices ($205,362) compared to places like the state capital, Madison ($390,755), or Lake Geneva ($362,319). However, this decrease in development is contributing to a more expensive housing market for prospective home buyers.

“Wisconsinites enjoyed a boom in their housing market in 2021, but by 2022, that boom led to tighter inventory and higher pricing for homes overall,” explains Gary Herman, President of Consolidated Credit. “Homebuyers bide their time while taking steps to minimize their credit card debt so they can compete in this market.”

Talk to a HUD-certified housing counselor to customize a homebuying action plan today.

Wisconsin has a $75,000 homestead exemption to protect home equity. If you are married and filing bankruptcy jointly, that amount is doubled to $150,000.

Median monthly owner costs, including mortgage: $1,602

Median gross rent payment: $992

If you are finding it challenging to make rental payments, you can seek assistance through Wisconsin’s rental programs. Wisconsin offers a lending hand through the Wisconsin Housing Assistance program for those seeking mortgage relief.

Retirement in Wisconsin

CNBC reported in 2024 that the average Wisconsin resident would need about $56,130 a year to retire. A 20% comfort buffer ($11,226) is recommended. That means the target for a comfortable retirement in Wisconsin would be about $67,356.

Exquisite lakes and forests, as well as the presence of all four seasons and an affordable lifestyle, draw people to Wisconsin. But unfortunately, the state income tax rate (3.5%-7.65%) may draw people away from retirement here. And when you consider that nearly one in seven retirees rely on Social Security for at least 90% of their income, it’s no surprise people may consider states with no income taxes before considering a state with income taxes.

Average Wisconsin insurance premiums

Wisconsin, similar to most states across the U.S., operates under a tort system, or a fault-based system when it comes to car accidents. That means the person determined to be “at fault” for causing any collision will also be responsible for the other person’s. That’s why it’s important you have coverage insurance. The average annual auto insurance premium for full coverage in Wisconsin is $1,839.

Regarding average health insurance premiums, expect to fork out a hefty $6,503 annually. As for home insurance, if the home is under $300,000, the average Wisconsinite is paying $1,176 per year for dwelling coverage.

The Census Bureau reports that 283,767 veterans live in Wisconsin. These resources are available to help Veterans that are facing unemployment, homelessness, and other hardships.

How Consolidated Credit helps Wisconsin residents find debt relief

In 2024, Consolidated Credit provided free credit counseling services to 2,231 credit users in the state of Wisconsin. Of those, 463 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $12,798). Those who did not enroll received a free debt analysis and complementary budget evaluation and were directed to the right solutions for their respective situations.

Relief options to consider if you’re in debt in Wisconsin

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you can refinance your debt at a low-interest rate and enjoy one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Wisconsin residents with high debt and a good credit score.

Wisconsinite homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Wisconsin residents with counseling programs that identify the best way to get out of debt after considering their situations. Wisconsin residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Wisconsin, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Wisconsinites can get out of debt in 36-60 payments, on average.

Another option for Wisconsin residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Wisconsinite residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below, you will find a few case studies from clients that we’ve helped in Wisconsin. If you’re facing challenges with debt, call us at (844) 276-1544to receive a free debt and budget evaluation from a certified credit counselor.

Don’t let credit card debt hold you back. Find the best debt relief option for you and join other Wisconsinites who eliminated their debt.

“I’ve had excellent communication with the staff. Every time I’ve spoken with a credit counselor they have been very helpful and courteous.

”

Where

she

started:

Total unsecured debt: $31,549.00

Estimated interest charges: $17,923.80

Time to payoff: 13 years, 8 months

Total monthly payments: $1,265.00

After DMP enrollment:

Average negotiated interest rate: 4.14%

Total interest charges: $3,267.38

Time to payoff: 4 years, 7 months

Total monthly payment: $635.00

Time Saved

9 years, 1 month

Monthly Savings

$630.00

Interest Saved

$14,656.42

Case Study

Terry

from

Milwaukee, WI

“It would have taken us at least 15 years to pay off our debt or we most likely would have had to declare bankruptcy. I’m so glad I paid attention to that commercial. I recommended them to a coworker and she is very pleased also. Thank you so much!

”

Where

he

started:

Total unsecured debt: $22,802.00

Estimated interest charges: $12,931.02

Time to payoff: 13 years, 8 months

Total monthly payments: $915.72

After DMP enrollment:

Average negotiated interest rate: 4.33%

Total interest charges: $2,563.31

Time to payoff: 3 years, 9 months

Total monthly payment: $516.00

Time Saved

9 years, 11 months

Monthly Savings

$354.72

Interest Saved

$10,367.71

Case Study

Wendy

from

Port Washington, WI

“I have nothing but wonderful things to say about Consolidated Credit – from the beginning when I felt so embarrassed to be calling, you made me feel at ease. It’s taken less than five years to become debt free and that is a HUGE accomplishment.

”

Where

she

started:

Total unsecured debt: $54,063.00

Estimated interest charges: $31,173.09

Time to payoff: 15 years, 11 months

Total monthly payments: $2,162.52

After DMP enrollment:

Average negotiated interest rate: 7.39%

Total interest charges: $5,653.13

Time to payoff: 4 years, 6 months

Total monthly payment: $1,118.00

Time Saved

11 years, 5 months

Monthly Savings

$1,044.52

Interest Saved

$25,519.96

It’s time to find relief from credit card debt! Get a free debt and budget evaluation from a certified credit counselor today and find out if you qualify for a debt relief program.