Find out how Consolidated Credit can help you!

Alabama Debt Relief Guide

Alabama, colloquially known as the “Cotton State,” ranks 4th on MERIC’s cost of living index for the second quarter of 2024. The index tracks the average costs of consumer goods and services that are needed to meet basic standard of living, meaning Alabama is one of the most affordable places to live in the U.S.

Recently, the state experienced a record low of unemployment. Boasting some of the most affordable places to live in the country, new homeowners have still found it tough to find a new home, much like the rest of the country.

“As budgets get squeezed, keeping credit card balances low is important to stay on budget,” says Gary Herman, President of Consolidated Credit. “That’s particularly important for people looking to buy a home to pay off debt so they can succeed in such a highly competitive housing market.”

The latest available data says that the average Alabama household has $10,248 in credit card debt. Citizens in Alabama collectively owe $18,068,853,153, an increase of $504,275,920 from the beginning of the year.

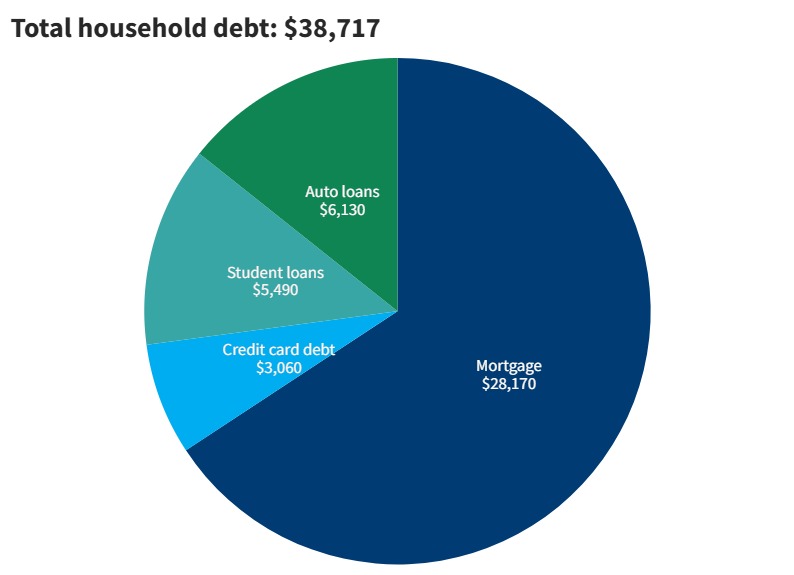

Consumer Debt in Alabama

This chart shows a breakdown of average consumer debt in Alabama, based on the latest Household Debt report from the Federal Reserve.

The latest available data shows 17,877 Alabamians filed for bankruptcy this year.

Income and employment in Alabama

Alabama’s per capita, or average per-person income, is $33,344, just short of the nationwide average of $41,261. The median household income is $59,609. And their minimum wage is on par with the federal minimum wage of $7.25 per hour.

With Alabama being a right-to-work state, it is “the public policy of Alabama that the right of persons to work shall not be denied or abridged on account of membership or non-membership in any labor union or labor organization.” Alabama has had this statute in its state code since 1953.

Alabama has a high poverty rate (15.6% in 2023, the latest available data). The Institute of Policy Studies, in its “Poor People’s Campaign” to get people to vote, wrote that 1.9 million poor and low-income Alabamians make up 47% of the electorate.

Apply for unemployment benefits in Alabama »

Unemployment Benefits:

- Minimum per Week: $45

- Maximum per Week: $275

- Maximum availability of benefits: 26 weeks

General Information about the Unemployment Insurance Program:

To file a UI claim online:

Alabama Department of Labor Initial Claim for Unemployment Compensation

To file a claim by telephone number:

Alabama Department of Labor Telephone Numbers

Job Centers:

Banking and taxes in Alabama

Alabama has an income tax range of 2% to 5% and a state sales tax of 4%. However, that sales tax rate can jump up to 7.5% if you are in the Banks zip code (36005). An alternative sales tax rate of 9% applies in the tax region Pike, which also belongs to the 36005 zip code.

Banking is also fairly uncommon compared to most states. Residents without a checking or savings account represent 7.6% of the population.

Alabama housing market

The median home price in Alabama is around $245,677. 57.4% of homes were sold under list price, meaning that prices are usually negotiated down after they’re listed, indicating a buyers’ market. Inventory is high and available, competition is low, and median home prices are below the national median.

However, this is not true for Birmingham, which is still considered a seller’s market. Birmingham’s poverty rate is 26.1%, which is 107% higher than the national average. The lack of available affordable housing is the difference between Birmingham and most of Alabama. However, the entire state, including Birmingham, is affected by low-wage jobs, declining industries like manufacturing, and limited access to quality education and healthcare.

Alabama offers a homestead exemption up to $15,000, doubling that for married couples, joint owners, or joint filing spouses.

- 73.8% of Alabamians are homeowners

- Median mortgage payment: $1,200

- Median rent payment: $1,400

- Average mortgage balance (debt): $171,883

If you are having trouble making rental payments, you can seek assistance through Alabama’s rental programs.

Alabama offers a lending hand for those seeking mortgage relief through Mortgage Assistance Alabama.

Consolidated Credit Helps Alabama Residents Reduce Their Credit Card Payments by Up to 50%

Retirement in Alabama

With a cost of living 12% below the national average and the second-lowest property taxes in the U.S., Alabama was named the 2nd best state for retirement by a CreditDonkey study. It is debated how much money is needed for retirement. Some experts say 70-80% of your job income must be withdrawn from your bank account annually to live comfortably. The median household income in Alabama is $59,609, so going by that equation, Alabamians will need about $42,000- $48,000 a year to retire comfortably.

Alabama’s highest state income tax rate is only 5%, and Social Security income from traditional pension plans is exempt from income tax. All homeowners 65 or older with an annual adjusted gross income of less than $12,000 are exempt from state property taxes.

Average Alabama insurance premiums

Nearly 20% of residents in Alabama are driving uninsured, ranking Alabama 7th in the nation for the highest number of uninsured drivers. The average yearly cost for auto insurance premiums in Alabama is $2,115. Insurance in Alabama is crucial as it is an “at-fault” state, meaning the insurance company of the person found at fault for the accident must pay for property damages, medical bills, etc.

The average homeowner insurance premiums in Alabama are $2,745 per year, which is slightly higher than the national average of $2,285.

Approximately 300,000 Alabama residents fall into the healthcare gap. The average Alabamian spends $5,952 a year on health insurance.

Helpful resources for Alabamians facing hardship

Food Insecurity

| City/Region | Food Bank | Phone Number | Address |

| Auburn | Food Bank of East Alabama | 334-821-9006 | 355 Industry Drive Auburn, AL 36832 |

| Birmingham | Community Food Bank of Central Alabama | 205-942-8911 | 107 Walter Davis Drive, Birmingham, AL 35209 |

| Huntsville | Food Bank of North Alabama | 256-539-2256 | 2000 B. Vernon Ave., Huntsville, AL 35805 [P.O. Box 18607] |

| Montgomery | Heart of Alabama Food Bank | 334-263-3784 | 521 Trade Center Street, Montgomery, AL 36108 |

| Theodore | Feeding the Gulf Coast | 251-653-1617 | 5248 Mobile South Street, Theodore, AL 36582 |

Veterans

As of 2024, Alabama is home to 359,506 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

Alabama Department of Veterans Affairs

Telephone: 334-242-5077

Find Veterans’ services in your area >>

Helpful employment resources for Veterans:

- CareerOneStop

- VeteranRecruiting.com

- Helmets to Hardhats

- Hiring Our Heroes

- My Next Move

- Warriors to Work

How Consolidated Credit helps Alabamians find debt relief

In 2024, Consolidated Credit provided free credit counseling to 2,897 Alabama residents. Of those, 325 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $12,953). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution to get out of debt as quickly as possible.

We’d also like to congratulate the 142 Alabama residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Alabama

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you can refinance your debt at a low-interest rate and enjoy one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Alabama residents with high debt and a good credit score.

Alabama homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Alabama residents with counseling programs that identify the best way to get out of debt after considering their situations. Alabama residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Alabama, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Alabamians can get out of debt in 36-60 payments, on average.

Another option for Alabama residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Alabama residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below are a few case studies from clients we’ve helped in Alabama. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

If you’re tired of making payments and getting nowhere, talk to a certified credit counselor to review your options for debt relief.

Get the debt relief you need! Talk with one of our certified credit counselors today to get a free debt and budget evaluation and find out if you qualify for a debt relief program.