In the early days of the state, Arizona’s economy relied on the five C’s: Copper, cotton, cattle, climate, and citrus. Arizona produces nearly two-thirds of all U.S. copper and is among the top five leading cotton states. And with more than 300 days of sunshine and the Grand Canyon, Arizona pulls in tourists and snowbirds. Still, Arizonans struggle with debt. The latest available data ranks Arizona 22nd in credit card debt amount – an average of $7,067.

“Phoenix has seen a rapid rise in demand for housing while facing property shortages, which is causing an increase in pricing,” says President of Consolidated Credit, Gary Herman. “On top of already facing a higher-than-average unemployment rate, minimizing or eliminating debt has become an ever-present cause for concern for Arizona residents.”

The latest available data says that the average household in Arizona has $11,298 in credit card debt. Citizens in this state collectively owe $28,224,946,525, an increase of $787,718,000 from the beginning of the year.

Consolidated Credit Helps Arizona Residents Reduce Their Total Credit Card Payments by Up to 50%

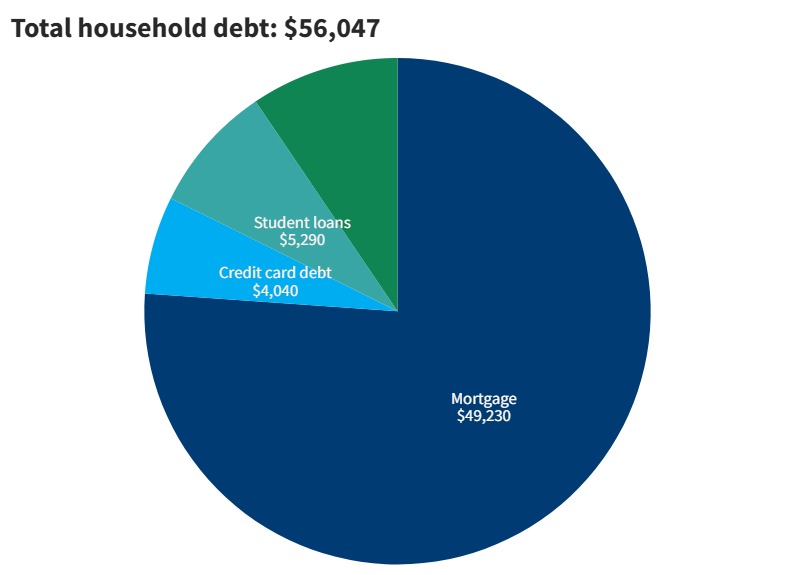

This chart breaks down the average consumer debt in Arizona based on the latest Household Debt report from the Federal Reserve.

The latest available data shows that 9,601 Arizonans filed for bankruptcy in 2024, compared to the previous year’s total of 16,933.

Income and employment in Arizona

Since Arizona is a right-to-work state. That means should employees decide to unionize, individuals are by law guaranteed the right to decline union membership and avoid paying dues. If someone is already a member and wants to resign from their union, they would not be fired due to the resignation.

Additionally, Arizona is an employment-at-will state. Therefore, consider employment a contract that can be severed at any time. As such, employees and employers do not guarantee they will uphold employment and can terminate their relationship as they wish.

These two factors give Arizona workers flexibility and opportunity but less job and salary security. So, it’s important that workers be proactive about securing raises and protections in case they are let go.

Arizona’s unemployment rate will be 3.5 percent in 2024. It ties Utah for 24th nationally, meaning only 26 states have higher unemployment than Arizona.

Arizona has an income tax rate of 2.59-4.5% and a state sales tax of 5.6%. However, with local taxes, sales tax can range between 5.6% and 11.2%, depending on the city. For example, in Navajo County, Winslow has one of the highest sales taxes at 9.43%, whereas Woodruff has one of the lowest at 6.43%.

Banking remains fairly common as the percentage of residents without a checking or savings account is a meager 3.6%.

Arizona housing market

Phoenix, Tucson, and Scottsdale remain the most sought-after cities in Arizona. The metropolitan Phoenix area is experiencing increasing demand for housing while struggling to meet expectations with a low inventory. As of May 2024, Phoenix is still a seller’s market, meaning demand for housing is higher than the inventory of available homes.

If and when you find it challenging to make rental payments, refer to Arizona’s emergency rental assistance program for support. Arizona offers a lending hand for those seeking mortgage relief through its “Save Our Home” program.

Talk to a HUD-certified housing counselor to get help with the housing challenges you’re facing

Ironically, Arizona’s motto, “Ditas Deus,” meaning “God enriches,” is seemingly code for moving to Mexico to enrich one’s life post-retirement. The average Arizonan must save $1,062,468 to continue living comfortably in retirement, which is 0.9% less than the national average.

Although Arizona has a warm climate, the increasing cost of living in metropolitan areas often leads to migration. As a result, Arizonans may consider moving to other states due to their affordability. And for the 45% of Arizonan retirees relying on Social Security for at least half of their income, a low cost of living is the biggest draw.

Average Arizona insurance premiums

Like most states across the U.S., Arizona operates under a fault-based system regarding car accidents. Arizona’s average auto insurance premiums are $2,737 yearly. Since insurance is so expensive, it is important for injury and property damage victims to have proof of liability to be compensated for their losses.

The latest available data shows that Arizona is home to 454,620 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

How Consolidated Credit helps Arizona residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 4,094 Arizona residents. Of those, 752 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $12,995). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution for their situation to get out of debt as quickly as possible.

We’d also like to congratulate the 265 Arizona residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Arizona

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you’ll get a low-interest rate for a loan that refinances all of your debt with one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Arizona residents with high debt and a good credit score.

Arizonian homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Arizona residents with counseling programs that identify the best way to get out of debt after considering their situations. Arizona residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Arizona, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Arizonians can get out of debt in 36-60 payments, on average.

Another option for Arizona residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Arizona residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below are a few case studies from clients we’ve helped in Arizona. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

Don’t let high interest rate credit card debt hold you back! Talk to a certified credit counselor to understand your options for debt relief

“The customer service agents are SOOO helpful and professional. Thanks so much for all your help!

”

Where

she

started:

Total unsecured debt: $25,685.00

Estimated interest charges: $14,652.28

Time to payoff: 12 years, 7 months

Total monthly payments: $1,027.40

After DMP enrollment:

Average negotiated interest rate: 6.83%

Total interest charges: $2,805.79

Time to payoff: 3 years, 4 months

Total monthly payment: $651.00

Time Saved

9 years, 3 months

Monthly Savings

$376.40

Interest Saved

$11,846.49

Case Study

Patricia

from

Tuscon, AZ

“Everyone has been understanding, compassionate, professional, accommodating… just amazingly helpful.

”

Where

she

started:

Total unsecured debt: $21,019.00

Estimated interest charges: $11,599.74

Time to payoff: 11 years, 2 months

Total monthly payments: $840.76

After DMP enrollment:

Average negotiated interest rate: 5.00%

Total interest charges: $2,510.55

Time to payoff: 3 years, 6 months

Total monthly payment: $513.00

Time Saved

7 years, 8 months

Monthly Savings

$327.76

Interest Saved

$9,089.19

Case Study

Teresita

from

San Luis, AZ

“After a couple of weeks the calls from my creditors stopped. I have been in peace for the last two years thanks to this. I recommend it 100%.

”

Where

she

started:

Total unsecured debt: $14,216.00

Estimated interest charges: $7,644.24

Time to payoff: 11 years

Total monthly payments: $361.92

After DMP enrollment:

Average negotiated interest rate: 7.29%

Total interest charges: $1,616.21

Time to payoff: 4 years

Total monthly payment: $309.00

Time Saved

7 years

Monthly Savings

$52.92

Interest Saved

$6,028.02

Ready to see if you qualify for debt relief through Consolidated Credit? Talk to a certified credit counselor now for a free debt and budget evaluation.