It’s tough to keep up with costs when they continue to rise at exponential rates. Living paycheck-to-paycheck is stressful enough, but as prices increase it’s just not sustainable. That’s what happens when inflation rises. If it’s squeezing your budget, then it may be time to adjust your financial strategy.

A simple definition of inflation

To counteract something effectively, you need to understand it first. So, what is inflation exactly?

Inflation occurs when prices rise on most goods and services. It’s a large-scale increase across the board. You don’t just see one or two costs in your budget get more expensive. Instead, everything gets more expensive at once.

While it’s a fact of life that costs generally rise over time, a period of inflation leads to rapid increases that most people just can’t afford.

During an inflationary period, the purchasing power you have declines. Each dollar you earn buys less stuff. It takes more money to purchase the same everyday goods.

How do we measure inflation?

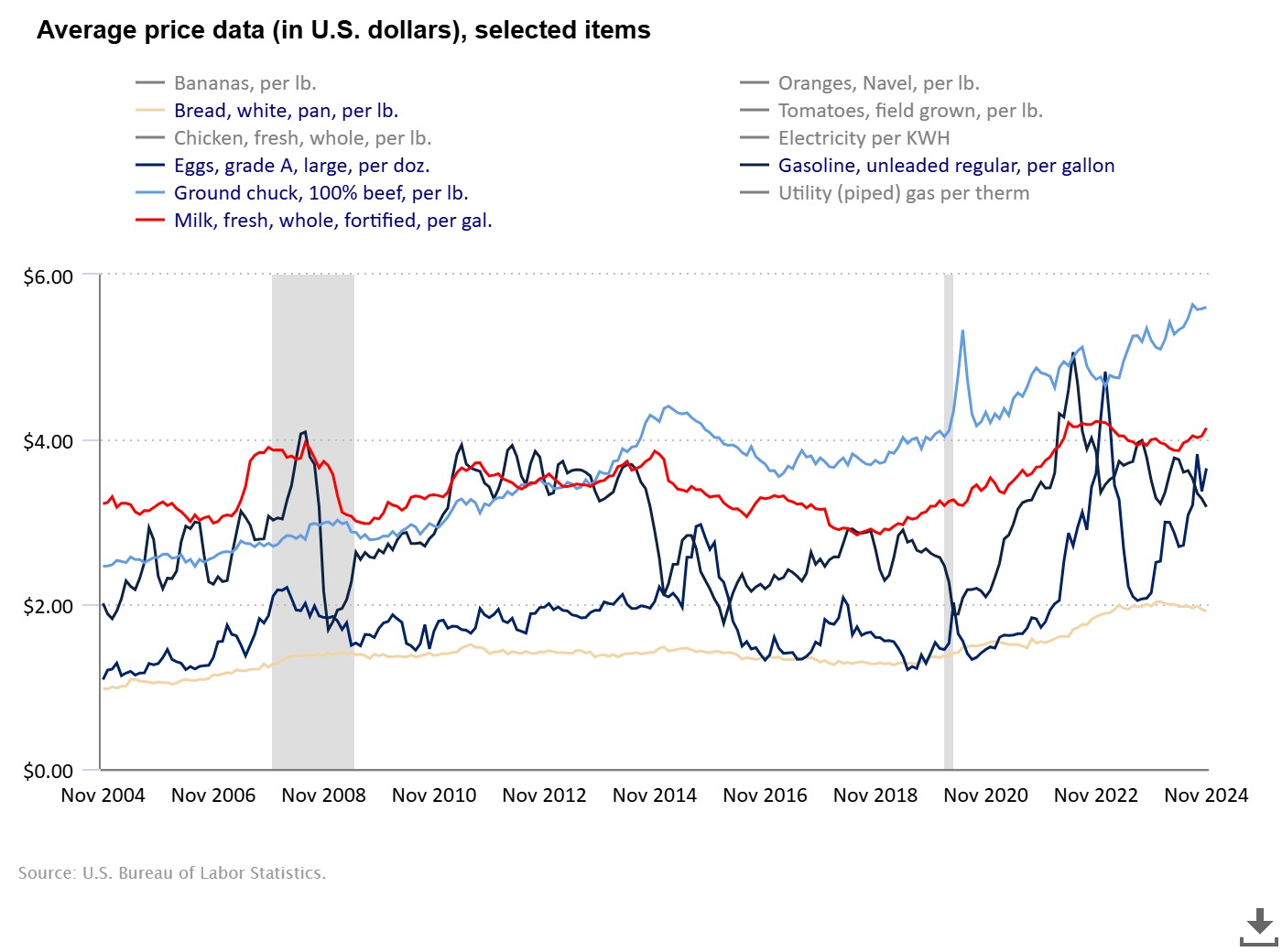

Inflation measures an increase in prices over time. How much those prices increase is known as the rate of inflation. It gets calculated by looking at the Consumer Price Index (CPI).[1] The U.S. Bureau of Labor Statistics (BLS) monitors prices that consumers pay for everything we buy and logs them over time in the CPI. Inflation measures the rate of increase in prices. If prices fall over time, then it’s known as deflation.

This chart shows the increases and decreases in prices over the past 20 years on key items that most Americans buy:

How bad is inflation right now?

The current annual inflation rate is 2.7%, which is comparable to levels last seen in early 2021.[2] Although inflation has eased from its 2022 peak, it continues to outpace pre-pandemic levels. This persistent price pressure means consumers pay substantially more for essential goods and services. While the overall economy may be stabilizing, the impact on household budgets remains a concern.

Ways to combat inflation

If you’re feeling the pinch of inflation, you’re not alone. While the economy has shown resilience, rising costs continue to impact many households. Here are some practical strategies to help you navigate these challenging times.

Budgeting during inflation

It’s always smart to audit your budget periodically. Goals and spending habits change over time. However, during periods of inflation, you must be proactive and adjust your budget accordingly.

- Start by checking your budgeting app or worksheet to see where you stand. Check the current cost of things like gas and groceries versus the actual costs paid over the past three months.

- If you spend more than you earn now, it’s time to make some tough choices and determine what you need to cut.

- Keep in mind that you should not budget down to the last dollar. You need breathing room. This includes saving 5%-10% of your income and having free cash flow. That’s money not allocated for saving or spending that you can use to cover unexpected expenses and ongoing price increases.

In normal circumstances, you only need to check your budget every few months once it’s set and balanced. However, it needs more attention during an inflationary period like this one. Check it every month.

A budgeting app can make this easier. Check with your bank or credit union first. They usually offer money management software that’s built into your accounts. That makes it easy to set spending limits and then get notified about overspending in real time. Use these alerts to your advantage.

Pay down credit card debt

Using credit cards to cover increasing costs is the opposite of what you should do during inflationary periods. Instead, focusing on paying off credit card debt would be best.

Each balance paid will eliminate one bill, freeing up more money to cover those rising costs. But a normal debt reduction plan won’t help if your budget is already tight. You simply don’t have the extra cash to make larger payments on your debts.

The good news is that there are ways to lower your total payments while you get out of debt. These solutions now offer budget breathing room and build more room over time.

These Options May be Able to Help

You can negotiate directly with creditors to pay off your balances. They may lower your interest rate, allowing you to pay off debt faster even with the same monthly payment. They may even lower your payments, although this usually means they will freeze your account so you can’t make new charges.

A debt consolidation loan is a personal loan you use to pay off your credit cards. It works because loans have much lower interest rates. In some cases, depending on the loan term you choose and how much you owe, you can lower your payments, too.

A debt management program (DMP) is a repayment plan designed for high interest rate credit card debt. A DMP reduces or eliminates interest and can reduce your total payments by 50%. The biggest advantage is that you can get lower rates even with bad credit.

Connect with a certified credit counselor to craft the best plan to pay off credit card debt.

Increase your income

The last way to fight inflation is the most obvious but not necessarily the easiest: increase your income.

You should talk to your boss about a raise if you’re employed. Get prepared by noting all the responsibilities you’ve taken on and achievements you’ve had since your last pay increase. If you get paid hourly wages, you can ask for more hours or work overtime.

You can also pick up a side gig. If you own a home, consider renting out an extra room.

Do whatever you can to increase how much you earn each month so you can offset cost increases. Still, if you’re like many people, increasing your income as much as you need may be difficult. People living on a fixed Social Security income may not have the means to increase their income.

Thus, it’s often best to budget around what you have and get a plan to pay down your debt first. Then, if you can increase your income, it will make those first two goals even easier. If you’re having trouble balancing everything in your budget, we can help. You can call (844) 276-1544 to get a free debt and budget analysis from a certified credit counselor. We can help you work through all these options and develop the best plan to get ahead of rising costs.

Sources

[1] U.S. Bureau of Labor Statistics – CPI

[2] Bankrate – Inflation slightly accelerated last month — here are the prices rising most