The “Centennial State” boasts low property taxes, low pension taxes, and 4.4% income taxes, making Colorado an attractive place to call home. But with home prices and housing costs skyrocketing rapidly and the same issues with inflation being felt throughout the nation, consumers are getting squeezed. That may explain why Colorado ranks 18th in “States with Largest and Smallest Credit Card Debt Increases.”

The average Colorado household owes $11,653 in credit card debt.

“Coloradoans are having a rough time with high credit card balances thanks to rising prices and unmanageable housing costs,” explains Gary Herman, President of Consolidated Credit. “Residents need to focus on getting debt-free with no credit card balances hanging over their heads. It’s the best way to combat inflation when it comes to your own household budget.”

Consolidated Credit Helps Colorado Residents Reduce Their Total Credit Card Payments by Up to 50%

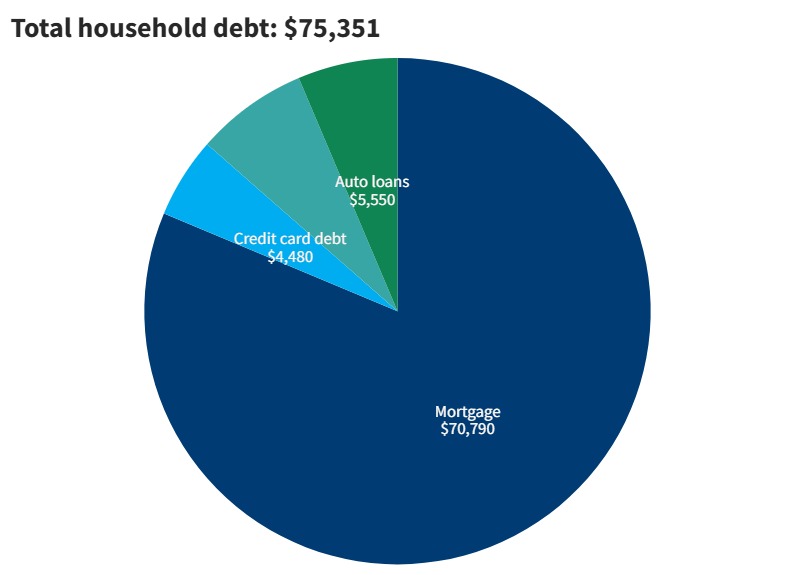

This chart breaks down the average consumer debt in Colorado based on the latest Household Debt report from the Federal Reserve.

The latest available data shows 6,152 Coloradans filed for bankruptcy last year.

Income and employment in Colorado

Colorado is not a right-to-work state. The state operates under a hybrid policy known as the Labor Peace Act. Under the Act, employees at most workplaces are not required to join a union or pay any union dues. Conversely, workers can still enjoy the same compensation and benefits as union members. However, non-union workers do not receive any union protections.

Colorado is an employment-at-will state. That means an employer can terminate employment anytime and for any reason. Similarly, employees can resign at any time and for any reason. Both the employer and employee do not guarantee they will uphold their end of an employment agreement.

In September of 2024, the unemployment rate in Colorado was 4%, which is very similar to the national unemployment rate of 4.1%.

Unemployment Benefits:

Minimum per week: $25

Maximum per week: $561 (low formula)/ $618 (high formula)

Colorado has a flat 4.4% individual income tax rate. The state imposes a state sales tax of 2.9%. The average combined state and local sales tax rate is 7.81%.

Banking is fairly common in Colorado much like the rest of the U.S. As of 2024, 6% of Coloradans are unbanked (meaning they don’t have a bank account), which is equal to the national average.

Colorado housing market

Colorado has a fairly expensive housing market. The Denver metro area is the country’s fifth least affordable housing market. In a 2024 report, Zillow reported a $542,000 median sale price, 8,521 new listings, and 26.6% of sales were over the list price.

The capital, Denver, has a median listing price of $597,962. Comparatively, Colorado Springs has a median home listing price of $465,000, while Boulder has a sky-high median listing price of $1,135,000.

Colorado currently has a homestead exemption of $250,000. This allows a homeowner to protect the value of their primary residence up to that amount.

CNBC reported in 2024 that the average Coloradan would need about $58,908 annually to retire. A 20% comfort buffer ($11,782) is recommended. That means the target for a comfortable retirement in Colorado would be about $70,689.

Colorado has the third lowest property taxes of any state. It also has low income and pension taxes, making it appealing to retirees. This is especially true when one in seven retirees rely on Social Security for 90% of their income.

Average Colorado insurance premiums

Colorado, much like most states in the U.S., operates under a fault-based system for car accidents. Basically, if you are “at fault” for causing a collision, you are responsible for the collision plus any other expenses. Auto insurance premiums are fairly high at $2,945.

Expect a hefty $3,222 annually for average annual home insurance premiums. Similarly, annual health insurance premiums are fairly standard at $6,451.

As of 2024, Colorado was home to 385,807 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

The Colorado Division of Veterans Affairs National crisis hotline: (800) 273-8255 Colorado Veterans Support Line: (844) 458-3760 Headquarters: 155 Van Gordon, Suite 201 (first floor) Lakewood, CO 80228

How Consolidated Credit helps Colorado residents find debt relief

In 2024, Consolidated Credit provided free credit counseling services to 2,808 credit users in Colorado. Of those, 790 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $13,590). Those who did not enroll received a free debt analysis and complementary budget evaluation and were directed to the right solutions for their respective situations.

We’d also like to congratulate the 287 Colorado residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Colorado

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you can refinance your debt at a low-interest rate and enjoy one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Coloradoan residents with high debt and a good credit score.

Coloradoan homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Colorado residents with counseling programs that identify the best way to get out of debt after considering their situations. Coloradoan residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Colorado, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Coloradoans can get out of debt in 36-60 payments, on average.

Another option for Colorado residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Coloradoan residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below are a few case studies from clients we’ve helped in Colorado. If you’re facing challenges with debt, call us at (844) 276-1544to receive a free debt and budget evaluation from a certified credit counselor.

Don’t waste another sleepless night stressing about your debt. Talk to a certified credit counselor to explore your options for debt relief.

“Consolidated Credit has helped me so much and in 4 years with less than one to go, most of the credit card debt I accumulated in a decade of overspending is gone and I’m almost debt free.

”

Where

she

started:

Total unsecured debt: $23,977.00

Estimated interest charges: $13,121.43

Time to payoff: 11 years, 11 months

Total monthly payments: $959.08

After DMP enrollment:

Average negotiated interest rate: 5.20%

Total interest charges: $2,684.55

Time to payoff: 4 years, 3 months

Total monthly payment: $529.00

Time Saved

7 years, 8 months

Monthly Savings

$430.08

Interest Saved

$10,436.88

Case Study

Kimberly

from

Boulder, CO

“I’ve been very happy with the services. You’re always helpful with excellent service and customer support. I’m really glad I found you and it’s comforting to know my credit card debt will be gone soon.

”

Where

she

started:

Total unsecured debt: $17,960.21

Estimated interest charges: $9,890.11

Time to payoff: 10 years, 10 months

Total monthly payments: $718.41

After DMP enrollment:

Average negotiated interest rate: 3.29%

Total interest charges: $1,181.93

Time to payoff: 4 years, 4 months

Total monthly payment: $370.00

Time Saved

6 years, 6 months

Monthly Savings

$348.41

Interest Saved

$8,708.18

Case Study

Michael

from

Arvada, CO

“I’m finally on the road to recovery! Thanks.

”

Where

he

started:

Total unsecured debt: $53,115.00

Estimated interest charges: $30,604.24

Time to payoff: 15 years, 5 months

Total monthly payments: $2,124.60

After DMP enrollment:

Average negotiated interest rate: 6.92%

Total interest charges: $9,937.81

Time to payoff: 4 years, 4 months

Total monthly payment: $1,218.00

Time Saved

11 years, 1 month

Monthly Savings

$906.60

Interest Saved

$20,666.43

Ready to see if Consolidated Credit’s debt management program can help you, too? Get a free evaluation from a certified credit counselor today.

This content is based on accredited financial data gathered from reputable sources, such as government websites, credit bureaus, and nonprofit organizations. All articles are written by certified credit counselors and fact checked by certified financial experts.

Our team strives to provide educational content that fully informs readers of all their options as they relate to debt, credit and personal finance. Our goal is to give readers the information they need to make informed financial decisions on their own.

This article contains references that provide sources for the financial data we used. The numbers in brackets [1,2,3] are clickable links to each data source or study referenced.