Sandwiched between the Great Plains and the Midwest is the state of Nebraska. A strong economy and a low cost of living draw people into the Cornhusker State. Still, even though unemployment rates and cost of living are low, Nebraskans struggle with debt. The latest available data says that the average Nebraska household has $9,195 in credit card debt. Citizens in this state collectively owe $6,511,364,323, an increase of $181,722,891 from the beginning of the year.

“Nebraska residents are getting hit with rising prices like the rest of the country,” says Gary Herman, President of Consolidated Credit. “And economic stability often means consumers get comfortable carrying credit card debt. I think that combination is why we’re seeing credit card balances rise in the state. But even if you’re stable, credit card debt isn’t good for your finances. You need to find a solution to pay it off.”

Consolidated Credit Helps Nebraska Residents Reduce Their Total Credit Card Payments by Up to 50%

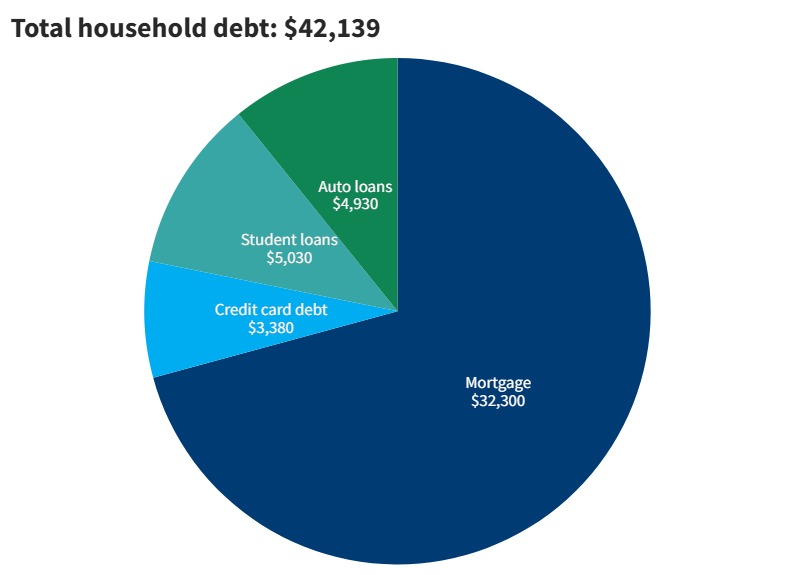

This chart shows a breakdown of average consumer debt in Nebraska based on the latest Household Debt report from the Federal Reserve.

In 2023, 2,359 Nebraskans filed for bankruptcy.

Income and employment in Nebraska

Nebraska has an average per capita (average per person) income of $38,585, which is slightly lower than the national average of $41,261. Nebraska has a median household income of $71,722. On top of this, Nebraska has a minimum wage of $12 compared to the federal minimum of $7.25.

Nebraska is a right-to-work state. This means that employees cannot be denied employment based on union status. And employees cannot be forced to join or leave a union. Employees are also not obligated to pay any union dues. However, employees are still allowed to enjoy any union benefits.

On top of this, Nebraska is an employment-at-will state. For this reason, employment may be terminated at any given moment and for any reason. Consequently, neither an employer nor an employee guarantee they will uphold employment. So, they may terminate their relationship in the same vein.

This freedom of employment gives Nebraska workers plenty of opportunity to seek any job placement and negotiate salary and benefits. But it can also mean less job security. This makes it crucial for Nebraskans to maintain a strong financial safety net, with robust emergency savings and low credit card balances.

Nebraska is on the lower end of unemployment, with an impressive percentage of 2.7%. Currently, the lowest unemployment rate in the country is 2% and the highest is 5.6%.

Nebraska has an income tax rate ranging between 2.46% and 5.84%. Nebraska imposes a state sales and use tax of 5.5%. Counties and cities in Nebraska are allowed to charge additional sales tax on top of the state sales tax.

For example, the state capital, Omaha, has a local tax of 2.5% on prepared foods and drinks.

Banking in Nebraska is also somewhat uncommon compared to most states, as residents without a checking or savings account represent 6.5% of the population.

Nebraska housing market

For Nebraskans trying to live in metropolitan areas, like Omaha and Lincoln, it can be expensive. However, the houses there are more reasonably priced than a lot of other high demand places in the United States. For example, Lincoln has a median home listing price of $275,741 , with homes spending an average of 14 days on the market. Still, it is crucial for first-time homebuyers to have a good handle on their finances so they can be mortgage-ready.

For homeowners, Nebraska offers homestead exemptions of up to $60,000.

Median monthly owner cost including mortgage: $1,612

Median gross rent payment: $987

If you are finding it challenging making rental payments, you can seek assistance through Nebraska’s emergency rental assistance program. For those seeking mortgage relief, Nebraska offers a lending hand through Nebraska Investment Finance Authority’s (NIFA) homebuyer programs.

Talk to a HUD-certified housing counselor to get help with the housing challenges you’re facing

CNBC reported in 2024 that the average Nebraska resident would need about $54,047 a year to retire. A 20% comfort buffer ($10,809) is recommended. That means the target for a comfortable retirement in Nebraska would be about $64,856.

Nebraska’s harsh winter climate and location in Tornado Alley may be drawbacks to retiring in the state. But, because Nebraska has low income tax rates, people often consider Nebraska an option. And for the retirees who rely on Social Security for most of their income, this is a huge draw to retiring in the state.

Average Nebraska insurance premiums

Nebraska, like most states across the U.S., operates under a fault-based system when it comes to car accidents. The average yearly auto insurance premiums are $2,316. That’s why it is imperative for injury and property damage victims to have proof of liability so they can be adequately compensated for their losses.

The average annual home insurance premiums are fairly high as well, at $2,304. And when it comes to average health insurance premiums, Nebraskans typically pay $6,426.

According to the Census Bureau, Nebraska is home to 109,982 Veterans. These resources are available to help Veterans that are facing unemployment, homelessness, and other hardships.

How Consolidated Credit helps Nebraska residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 864 Nebraska residents. Of those, 44 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $10,525). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution for their situation to get out of debt as quickly as possible.

We’d also like to congratulate the 54 Nebraska residents that got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Nebraska

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you can refinance your debt at a low-interest rate and enjoy one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Nebraska residents with high debt and a good credit score.

Nebraskan homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Nebraska residents with counseling programs that identify the best way to get out of debt after considering their situations. Nebraska residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Nebraska, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Nebraskans can get out of debt in 36-60 payments, on average.

Another option for Nebraska residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Nebraskan residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below, you will find a few case studies from clients that we’ve helped in Nebraska. If you’re facing challenges with debt, call us at (844) 276-1544to receive a free debt and budget evaluation from a certified credit counselor.

Ready to see if Consolidated Credit can help you, too? Connect with a certified credit counselor now for a free debt and budget evaluation

“My experience with Consolidated has been excellent. I have one payment remaining and then I’ll have fully paid off $54,000 in debt.

”

Where

he

started:

Total unsecured debt: $54,000.00

Estimated interest charges: $31,641.24

Time to payoff: 17 years, 2 months

Total monthly payments: $2,160.00

After DMP enrollment:

Average negotiated interest rate: 8.00%

Total interest charges: $9,954.33

Time to payoff: 4 years, 4 months

Total monthly payment: $1,230.00

Time Saved

12 years, 10 months

Monthly Savings

$930.00

Interest Saved

$21,686.91

Case Study

June

from

Omaha, NE

“Consolidated Credit helped me pay off a lot of my credit card debt in a considerably short period of time. I was very happy with how professional and knowledge all of the reps were in helping me get my debt under control.

”

Where

she

started:

Total unsecured debt: $37,504.00

Estimated interest charges: $22,123.01

Time to payoff: 16 years

Total monthly payments: $1,500.16

After DMP enrollment:

Average negotiated interest rate: 6.33%

Total interest charges: $5,512.75

Time to payoff: 4 years, 3 months

Total monthly payment: $859.00

Time Saved

11 years, 9 months

Monthly Savings

$641.16

Interest Saved

$16,610.26

This content is based on accredited financial data gathered from reputable sources, such as government websites, credit bureaus, and nonprofit organizations. All articles are written by certified credit counselors and fact checked by certified financial experts.

Our team strives to provide educational content that fully informs readers of all their options as they relate to debt, credit and personal finance. Our goal is to give readers the information they need to make informed financial decisions on their own.

This article contains references that provide sources for the financial data we used. The numbers in brackets [1,2,3] are clickable links to each data source or study referenced.