Alaska is considered one of the most expensive states to live in. For one, it is miles away from the “lower” 48 states, which makes it harder to import consumer goods. Thankfully, Alaskans have access to Permanent Fund Dividend checks to offset the higher cost of living, as well as no state or income tax.

However, even with those added financial perks, Alaskans still struggle with debt. Alaskans have more credit card debt than consumers in any other state, with an average balance of $6,617.

“Many credit users in Alaska are getting to a point where their debt levels are simply unsustainable,” says Gary Herman, President of Consolidated Credit. “At a certain point, you simply won’t be able to keep up with the bills and maintain a balanced budget. For Alaskans facing these types of debt levels, it’s critical that they develop the right plan to pay off their debt.”

The latest available data shows that the average Alaskan household has $13,624 in credit card debt. Citizens in this state collectively owe $3,285,148,519, an increase of $91,683,810 from the beginning of the year.

Consolidated Credit Helps Alaska Residents Reduce Their Total Credit Card Payments by Up to 50%

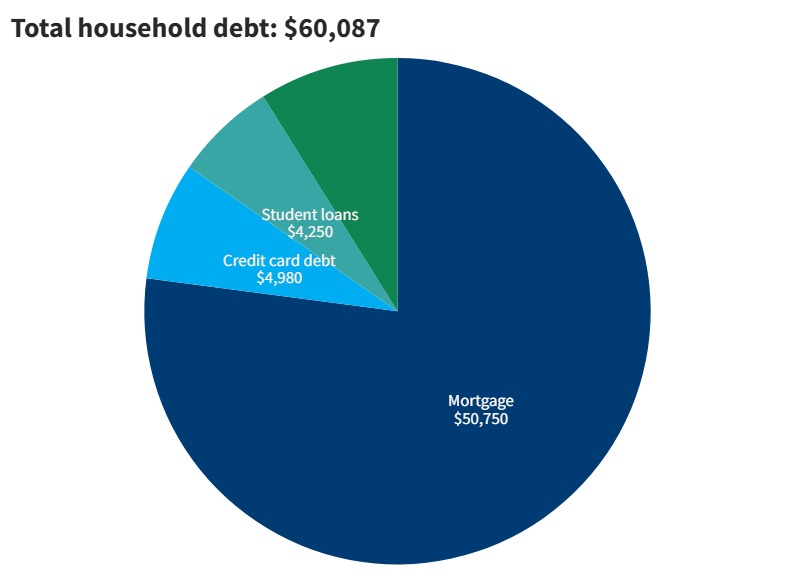

This chart breaks down the average consumer debt in Alaska based on the latest Household Debt report from the Federal Reserve.

The latest available data shows 212 Alaskans filed for bankruptcy this year.

Income and employment in Alaska

With a per capita (average per person) income of $42,828, Alaskans are faring alright, considering the national average is $41,261. They also have a median household income of $86,370. Their minimum wage will be $15 an hour by 2027, which is fairly higher than the $7.25 federal minimum wage.

Since Alaska is not a right-to-work state, employees can choose whether to join a union or not. Union members may also resign. Non-members must only proportionately pay for their part of a union’s proven bargaining costs.

Additionally, non-members may not be forced to pay any fees until the costs have been stated. And even then, the individual can challenge the costs provided by the union.

Furthermore, Alaska is an employment-at-will state. This means that employment may be terminated at any moment and for any reason. Neither the employer nor the employee guarantees they will uphold employment. Hence, they may also terminate their relationship in a similar fashion.

Those two facts together mean Alaskans have great job opportunities and career flexibility. However, residents can also be undercut on income and have less job security.

Parts of Alaska currently have some of the highest unemployment in the nation.

Kusilvak, Alaska’s unemployment rate is 15.1%, compared to the 2024 national rate of 4.1%.

Alaska has no income tax rate and no state sales tax. The average total state and local tax burden for Alaskans is 1.82%, the lowest among the fifty states.

Additionally, all Alaskan residents receive annual payments from the Alaska Permanent Fund Corp, which are made up of revenue and investment earnings from mineral lease rentals and royalties.

Banking is also fairly common compared to most states. Only 3% of the population has no checking or savings account.

Alaska housing market

For many Alaskans, buying a home in a seller’s market has been frustrating. Anchorage is the largest and most populous city in Alaska, accounting for 40% of the state’s population.

Unsurprisingly, that means Anchorage has a highly competitive housing market, with prices well above average Alaskan housing prices. Anchorage’s median home listing price is $373,799. By contrast, the second most populous city of Fairbanks has a median home listing price of $296,511.

Anchorage, Alaska, is a balanced market, meaning the supply and demand of homes are about the same.

You can file for bankruptcy in Alaska after living there for over 180 days. However, to use the exemptions, you must live in the state for at least 730 days in Alaska before filing. Otherwise, you would use your previous state’s exemptions.

CNBC reported in 2024 that the average Alaska resident would need about $72,390 annually to retire. A 20% comfort buffer ($14,478) is recommended. That means the target for a comfortable retirement in Alaska would be about $86,868.

Though Alaska’s climate and its cost of living – mostly due to Alaska’s remote location – may turn people away from retiring in the state, its tax rates continue to turn people’s heads. And for the retirees relying on their Social Security for at least 90% of their income, the fact that Social Security income is not taxed remains a huge draw to retiring in the state.

Average Alaska insurance premiums

As is the case with most states across the U.S., Alaska operates under a fault-based system when it comes to car accidents. For this reason, along with an average of $2,311 yearly for auto insurance premiums, it is essential that victims have proof of liability for injury and property damage so they may be compensated for their losses.

On the other hand, average annual home insurance premiums are fairly low at $986 for $300,000 of dwelling coverage. But regarding average health insurance premiums, expect to fork out about $9,356 annually.

According to the Census Bureau, Alaska is home to 53,692 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

Unemployment Benefits:

Minimum per week: $56

Maximum per week: $370

Maximum availability of benefits: 26 weeks

General Information about the Unemployment Insurance Program:

How Consolidated Credit helps Alaska residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 310 Alaska residents. Of those, 34 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $13,887). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution to get out of debt as quickly as possible.

We’d also like to congratulate the 16 Alaska residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Alaska

If you have good credit and need to pay off credit card debt and other non-secured debts, a debt consolidation loan is an excellent option for you. By having good credit, you’ll get a low-interest rate for a loan that refinances all of your debt with one monthly payment. This will help you get out of debt faster, and you may wind up paying less each month. This is an excellent solution for Alaska residents with high debt and a good credit score.

Alaskan homeowners may qualify for a home equity loan or a home equity loan of credit, sometimes called a (HELOC). These types of loans use the equity in your home. Due to rapid home value increases, many residents have equity in their homes. The loan allows you to borrow against the equity in your home and pay off credit cards and other debt. This is not a step to take lightly because you could lose your home in foreclosure if you can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Consolidated Credit helps Alaska residents with counseling programs that identify the best way to get out of debt after considering their situations. Alaska residents can get a confidential debt and budget evaluation from a certified credit counselor. Afterward, the counselor will go over the available options and which course of action best meets a person’s needs and goals.

In Alaska, as in other states, it’s best to avoid bankruptcy. If you can afford to repay all that you owe to avoid credit damage but can’t do it on your own, a debt management program can help. You enroll through a credit counseling agency. The agency will work with your creditors to reduce or eliminate interest and work out a payment schedule. Qualifying Alaskans can get out of debt in 36-60 payments, on average.

Another option for Alaska residents is debt settlement. With debt settlement, you settle your debt independently or with the help of a debt settlement company. In this program, you agree to pay your creditors a portion of what is owed. This will damage your credit rating because you are not paying on the terms you first agreed to. Late payments, which are often part of this program, will hurt your credit rating for seven years. Even with those negatives, this can be an excellent program for Alaskan residents with overwhelming debt. It can help you avoid bankruptcy.

If you’re curious how we can help you, below are a few case studies from clients we’ve helped in Alaska. If you’re facing challenges with debt, call us at (844) 276-1544to receive a free debt and budget evaluation from a certified credit counselor.

If you’re tired of making payments and getting nowhere, talk to a certified credit counselor to review your options for debt relief.

“This has been a very good, professional solution to our problem. Everything was handled in a timely fashion and the results have been outstanding. I sincerely believe you cannot find any service that can compare with them.

”

Where

he

started:

Total unsecured debt: $28,814.34

Estimated interest charges: $16,023.73

Time to payoff: 14 years, 1 month

Total monthly payments: $1,152.57

After DMP enrollment:

Average negotiated interest rate: 11.28%

Total interest charges: $3,745.65

Time to payoff: 2 years, 9 months

Total monthly payment: $992.00

Time Saved

11 years, 4 months

Monthly Savings

$106.57

Interest Saved

$12,278.08

Case Study

Christopher

from

Palmer, AK

“The service has been great so far. Thanks!

”

Where

he

started:

Total unsecured debt: $24,111.00

Estimated interest charges: $13,201.86

Time to payoff: 12 years, 6 months

Total monthly payments: $964.44

After DMP enrollment:

Average negotiated interest rate: 7.93%

Total interest charges: $4,675.67

Time to payoff: 4 years, 6 months

Total monthly payment: $540.00

Time Saved

8 years

Monthly Savings

$424.44

Interest Saved

$8,526.19

Case Study

Lacey

from

North Pole, AK

“My husband and I only have 2 more payments and we’ll be debt free! Best decision ever! Thank you!

”

Where

she

started:

Total unsecured debt: $12,787.00

Estimated interest charges: $6,786.92

Time to payoff: 10 years, 9 months

Total monthly payments: $511.48

After DMP enrollment:

Average negotiated interest rate: 9.83%

Total interest charges: $3,128.92

Time to payoff: 3 years, 6 months

Total monthly payment: $367.00

Time Saved

7 years, 3 months

Monthly Savings

$144.48

Interest Saved

$3,658.00

Ready to see if Consolidated Credit can help you find debt relief, too? Get a free debt evaluation to find the best option to eliminate debt in your situation.

This content is based on accredited financial data gathered from reputable sources, such as government websites, credit bureaus, and nonprofit organizations. All articles are written by certified credit counselors and fact checked by certified financial experts.

Our team strives to provide educational content that fully informs readers of all their options as they relate to debt, credit and personal finance. Our goal is to give readers the information they need to make informed financial decisions on their own.

This article contains references that provide sources for the financial data we used. The numbers in brackets [1,2,3] are clickable links to each data source or study referenced.