Washington, DC was founded as the nation’s capital in 1790 and has since been at the heart of American politics and culture as it continues to evolve. This is one reason why it is not a cheap place to live. As of 2024, It ranks 50th on MERIC’s affordability scale. Only California and Hawaii surpassed D.C.’s cost of living.

“Washington, DC is doing relatively well now compared to other areas. It has a strong economy for most people, but affordability for rentals and owner-occupied homes in the District is proving challenging for potential homebuyers,” says Gary Herman, President of Consolidated Credit. “D.C. residents need to focus on financial fundamentals like maintaining a budget, minimizing debt, and maintaining good credit to get ahead in today’s economy.”

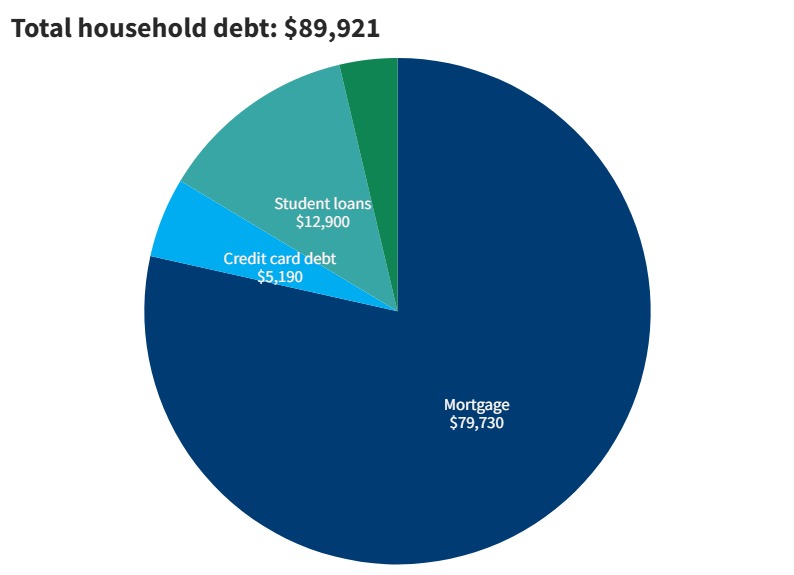

The latest available data says that Washington, DC has the highest credit card debt ($8,538 on average).

Consolidated Credit Helps Washington, DC Residents Reduce Their Total Credit Card Payments by Up to 50%

This chart breaks down the average consumer debt in Washington, DC, based on the latest Household Debt report from the Federal Reserve.

Roughly 388 D.C. residents filed for bankruptcy last year.

Income and employment in Washington, DC

Washington, DC is not a right-to-work “state,” in fact, D.C. is not a state at all, just a district. When a state (or district in this case) is not “right to work,” union dues are mandatory for employment. That’s even the case if the worker is not a part of the union.

Washington, DC typically experiences higher job growth than the nation as a whole. (Job growth refers to the number of nonfarm payroll jobs added to the economy in a month and is an important indicator of the economy’s health.). In 2023, however, the metropolitan Washington, DC area experienced stagnation. Total nonfarm employment only grew 0.7%, and total private employment 0.3%, from January 2023 to March 2024. This is below the national percentages of employment growth ( 2.2% nonfarm and 2% private) during the same period.

The District is also experiencing a labor shortage in 2024. Many industries have a mismatch between the worker supply and labor demand. As a result, there are 45 available workers for every 100 open positions, the labor force participation rate is 70.9, and the unemployment rate is 5.0.

Pay rates in the District of Columbia can be excellent, with an average per capita income of $71,297 and an average median household income of $101,722; even the minimum wage is high at $17.50. However, with the high cost of living and inequality so rampant, most D.C. residents do not reap the rewards of high pay. It still has one of the nation’s highest poverty rates at 14%.

When you’re unemployed in Washington, DC, you receive unemployment benefits from the District of Columbia. Typically Unemployment Insurance (U.I.) will last 26 weeks.

Washington, DC is an expensive city to live in. Maintaining basic living expenses despite high wages, especially rent or a mortgage, can be challenging. When that happens, sometimes people use credit cards to pay their bills. In this situation, maintain a budget and minimize high-interest-rate credit card debt.

Residents of our nation’s capital pay a state income tax of 4% to 10.75% and a district sales tax of 6%.

Taxes can be reduced by taking advantage of the Individual Income Property Tax Credit, which is available to homeowners and renters. First-time homebuyer tax credits and homestead deductions are also available.

Washington, DC does not have any tax-free holidays or periods. However, neighboring Virginia and Maryland have a few tax holidays, and residents can use the excellent Metro system to access shopping malls and other retail locations.

District residents are slightly less likely to bank than the average American. The percentage of unbanked residents without a checking or savings account is 8%.

Washington, DC housing market

Housing in the District of Columbia has been competitive as the city and metro area have grown. With relatively high salaries, residents of the District have been able to bid up prices for new homes and condos. However, this is pricing many new buyers out of the market. This is somewhat offset by the availability of more affordable housing in Maryland and Virginia, some of which have easy access from the Metro system.

Washington, DC residents can also take advantage of homestead deductions, including tax relief for senior citizens and disabled property owners.

Washington, C does have an emergency rental assistance program if you are facing difficulties making rental payments. Additionally, Washington, DC assists those with problems with their mortgage. For those who wish to purchase a home, many programs are sponsored by the District.

Talk to a HUD-certified housing counselor to get help with the housing challenges you’re facing

The District and the surrounding metro area feature many attractive options for retirees. Amenities include cultural events, fine dining, history, shopping, access to education, a large diversity of housing, excellent public transportation, and easy access to other metropolitan areas on the East Coast of the United States. The Washington, DC metro area features three airports, including one on the Metro train line and high-speed trains that make travel to New York, Philadelphia, and Boston quick and accessible. You could easily live in Washington, DC, or some of the surrounding areas and not need a car.

However, Washington, DC has a high cost of living, and retirement in The District of Columbia could be a challenge for those who are retired and on a fixed income. Other areas offer a much lower tax structure, less expensive housing, and a better climate. The average resident retires at age 67, leaving much time to enjoy the city. Many retirees live just outside of the Washington, DC borders where, in some instances, living costs are lower.

Average Washington, DC insurance premiums

Washington, DC is a no-fault district for auto insurance. The average driver has an auto insurance premium of $2,388 per year.

Homeowners’ insurance rates are reasonable and lower than the national average; insurance premiums are $1,377 annually. That could be due to a large number of condos and co-ops located in Washington, DC.

Health insurance premiums are lower than national averages. Only 2.9% of residents lack coverage, compared to the 8% who are uninsured nationally. The average cost of health insurance in D.C. is $9,040 per person.

Helpful resources for DC residents facing hardship

As of 2024, Washington, DC is home to 29,798 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

How Consolidated Credit helps Washington, DC residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 630 Washington DC residents. Of those, 78 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $16,062). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution for their situation to get out of debt as quickly as possible.

We’d also like to congratulate the 20 Washington, DC residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in The District of Columbia

A debt consolidation loan is an unsecured personal loan that you get to pay off credit cards and other existing debts. You need good credit to qualify for the lowest interest rate possible. That low rate helps lower your total payments so you can get out of debt faster, even though you may pay less each month. So, this is a good solution for Washington, DC residents with a high credit score.

A home equity loan or home equity loan of credit (HELOC) is a debt solution that’s only available to homeowners in Washington, DC . If you have equity available in your home, you can borrow against that equity and use the funds to pay off your debt. However, this can be a risky option for paying off credit card debt if you are living paycheck-to-paycheck. Home equity lending products put Washington, DC residents at risk of foreclosure if they can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Nonprofit credit counseling services like those provided by Consolidated Credit help Washington, DC residents identify the best solution for getting out of debt. This is a free service. Washington, DC residents can get a confidential debt and budget evaluation from a certified credit counselor. Then the counselor will explain options that are available to each person and recommend the best course of action based on an individual’s needs and goals.

If a Washington, DC resident cannot get out of debt effectively on their own but has the ability to repay everything they owe to avoid bankruptcy, a debt management program is often the best solution. You enroll in the program through a credit counseling organization. They help you find a monthly payment you can afford and then work with your creditors to reduce or eliminate interest. Qualifying Washington, DC residents can get out of debt in 36-60 payments.

Debt settlement allows Washington, DC residents to get out of debt for a percentage of what they owe. You can settle debt on your own and negotiate with individual creditors and collectors or enroll in a debt settlement program to get professional help. This does cause credit damage. Each debt settled will be noted on your credit report for seven years from the date the account first became delinquent. However, it can be a viable debt relief option for avoiding bankruptcy when you are completely overwhelmed with debt.

If you’re curious how we can help you, below are a few case studies from clients we’ve helped in Washington, DC. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

If you live in Washington, DC and are working to pay off credit card debt, we can help. Get a free evaluation from a certified credit counselor today.

“My interest rates were too high – 16, 17, 18 percent. Consolidated Credit was able to lower my rates to a point where my payments now go toward the principal so I can finally get out of debt. My credit score is going up, too! It was around 650 before but now it’s close to 700.

”

Where

she

started:

Total unsecured debt: $18,601.00

Estimated interest charges: $10,654.62

Time to payoff: 13 years, 8 months

Total monthly payments: $744.04

After DMP enrollment:

Average negotiated interest rate: 8.50%

Total interest charges: $3,680.08

Time to payoff: 4 years, 9 months

Total monthly payment: $390.00

Time Saved

8 years, 11 months

Monthly Savings

$354.04

Interest Saved

$6,974.54

Case Study

Maria

from

Lorton, VA

“If not for your persistence, I probably still wouldn’t be sleeping at night. It was hard at first, but when 2 or 3 of my credit cards were paid off it was an awesome feeling. Quick response and always there to assist. Thanks!

”

Where

she

started:

Total unsecured debt: $39,179.00

Estimated interest charges: $22,369.05

Time to payoff: 14 years, 3 months

Total monthly payments: $1,567.16

After DMP enrollment:

Average negotiated interest rate: 5.11%

Total interest charges: $1,920.78

Time to payoff: 4 years, 4 months

Total monthly payment: $798.00

Time Saved

9 years, 11 months

Monthly Savings

$769.16

Interest Saved

$20,448.27

Case Study

Aaron

from

Rockville, MD

“This is a great service!

”

Where

he

started:

Total unsecured debt: $44,198.00

Estimated interest charges: $25,759.74

Time to payoff: 14 years

Total monthly payments: $1,767.92

After DMP enrollment:

Average negotiated interest rate: 8.30%

Total interest charges: $8,385.72

Time to payoff: 4 years, 4 months

Total monthly payment: $1,016.00

Time Saved

9 years, 8 months

Monthly Savings

$751.92

Interest Saved

$17,374.02

Ready to see if Consolidated Credit can help you, too? Talk to a certified credit counselor to review your options for debt relief.