The average Virginia household has $12,011 in credit card debt, ranking the state at No.11 on WalletHub’s “States with Largest and Smallest Credit Card Debt Increases.”

Collectively, Virginians’ credit card debt is $36,039,634,018.

The “Old Dominion State” has changed in the past few decades. Coal production has rapidly declined since the 1990s, and tobacco farms are cutting back as cigarette demand declines.

At the same time, the Dulles tech corridor, second in size only to Silicon Valley, continues to grow and attract more leading tech companies. Additionally, military and defense-related industries and finance continue to grow.

“The economy of Virginia is in good condition compared to other states,” says Gary Herman, President of Consolidated Credit, “but rising housing costs are severely affecting urban areas, and energy costs are hurting consumers in rural areas. So, no matter where you live in Virginia, you may see your budget squeezed. Keeping credit card debt under control is essential in situations like these.”

Consolidated Credit Helps Virginia Residents Reduce Their Total Credit Card Payments by Up to 50% – Free evaluation

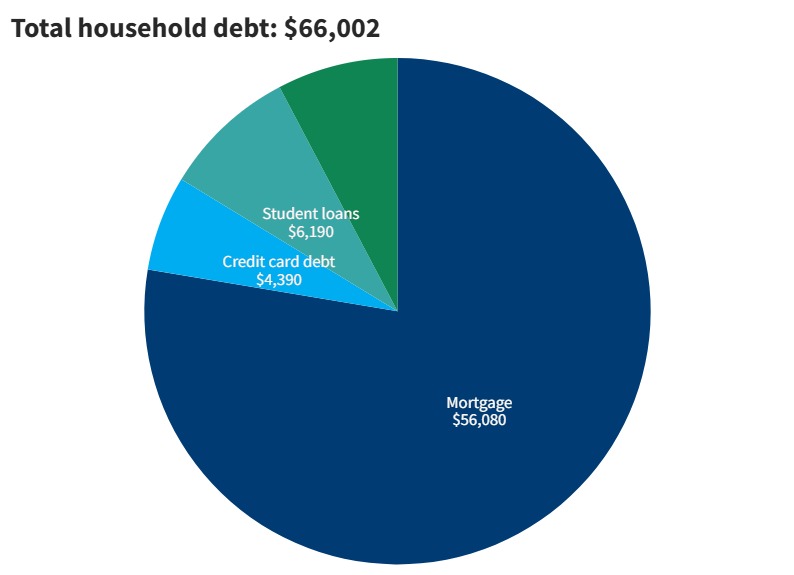

This chart breaks down the average consumer debt in Virginia, based on the latest Household Debt report from the Federal Reserve.

Income and employment in Virginia

Virginia is a right-to-work state. That means workers are not required to pay union membership dues, but they can choose to do so.

Virginia employers are adjusting to a job market where finding workers is challenging. With a sizable high-tech employment base and the need for qualified employees for security clearances, the competition for job candidates is challenging. Job growth in the state has been robust. From 2023-2024, the Virginia Employment Commission estimates that total nonfarm employment increased by 63,500 to create a total of 4,250,900 jobs; private sector employment increased by 56,200 to create a total of 3,506,100 jobs; and the government sector employment increased by 7,300 to create a total of 744,800 jobs.

Many military bases and installations in Virginia help stabilize jobs and the state economy. The Pentagon, located in Northern Virginia, employs over 23,000 federal and civilian employees. Norfolk Naval Station employs nearly 60,000 enlisted service people and around 20,000 civilian employees and contractors. Even the CIA has its headquarters in the state. While the number of employees at that facility is classified, it is still significant. Virginia has the second-largest active-duty military population after California.

Other major employers, such as Freddie Mac, General Dynamics, Northrop Grumman, and Capital One, all have headquarters in Virginia and offer high-paying careers. Those Fortune 500 companies take advantage of one of the highest-educated workforces in the nation. 49% of workers in Virginia have an associate degree or higher.

Virginia’s pay rates can be excellent. With an average per capita income of $47,210 and a median household income of $87,249, the minimum wage of $9.50 per hour is slightly above the nationwide minimum wage of $7.25.

Unemployment

Despite the tight labor market in Virginia, there are still unemployed people. If you are unemployed in Virginia, your Unemployment Insurance will last up to 26 weeks.

Virginia residents pay a variable income tax that ranges from 2-5.75%. Virginia does have tax reciprocity with four other states and Washington, DC. So, those residents pay taxes to their home states.

Virginia residents enjoy a three-day sales tax holiday in early August. During the holiday, taxes are not applied to clothing, school supplies, emergency products, and other categories. The sales tax in Virginia is 4.3%.

Virginia residents are also more likely to bank than the average American. Just 4% of unbanked residents have no checking or savings account.

Virginia housing market

As of 2024, Virginia is a seller’s market, where demand outweighs supply and housing prices are relatively high. Certain cities are seeing particularly high-cost increases. The median price of a home in Virginia Beach in May 2024 was $399,000, a 7.8% increase from 2023. Richmond had a more drastic increase of 19.3% from 2023 to 2024, with a median home price of $424,995.

Virginia residents can take advantage of homestead deductions. Other deductions are available for residents over 65 or permanently and totally disabled.

Virginia has help for renters who are having difficulty making their rent payments. Homeowners in Virginia can also get help with their mortgage payments. If you are considering buying a home in Virginia, many resources are available.

Talk to a HUD-certified housing counselor to get help with the housing challenges you’re facing.

CNBC reported in 2024 that the average Virginia resident would need about $58,618 a year to retire. A 20% comfort buffer ($11,724) is recommended. That means the target for a comfortable retirement in Virginia would be about $70,342.

Virginia has very favorable taxes for retirees, with all Social Security taxes exempt from the state income tax and additional age-related tax deductions. Crime rates are statistically low – Virginia has the lowest crime rate in the South Atlantic Region.

The “Old Dominion State” offers many amenities to retirees beyond low taxes and safety. The region has many historical sites, including some that date back before the Revolutionary War. Those over 60 can take many university courses for free, and if your income is below a certain threshold, you can even take those classes for academic credit. If you’re retired from the Military, you’ll find plenty of other Veterans. There is also a lot of public transportation in more urban areas and access to major cities up and down the East Coast.

Average Virginia insurance premiums

Virginia residents pay an average of $2,098 annually for full-coverage auto insurance. On average, homeowner’s insurance for a $300,000 home is around $1,546.

Health insurance in Virginia averages around $6,370 per person. Virginia residents are more likely to have health coverage than people from other states, with only 6.4% of residents lacking coverage. Nationally, 8% of Americans are uninsured.

Helpful resources for Virginia residents facing hardship

As of 2024, Virginia is home to 676,665 Veterans. These resources are available to help Veterans facing unemployment, homelessness, and other hardships.

Veteran Resources: National crisis hotline: (800) 273-8255

How Consolidated Credit helps Virginia residents find debt relief

In 2024, Consolidated Credit provided free credit counseling to 3,964 Virginia residents. Of those, 977 went on to consolidate their debt with our help through a debt management program (the average amount of debt enrolled was $13,978). The others received a free debt analysis and complementary budget evaluation, and they were directed to the right solution for their situation to get out of debt as quickly as possible.

We’d also like to congratulate the 335 Virginia residents who got debt-free last year with the help of Consolidated Credit!

Relief options to consider if you’re in debt in Virginia

A debt consolidation loan is an unsecured personal loan that you get to pay off credit cards and other existing debts. You need good credit to qualify for the lowest interest rate possible. That low rate helps lower your total payments so you can get out of debt faster, even though you may pay less each month. So, this is a good solution for Virginia residents with a high credit score.’

A home equity loan or home equity loan of credit (HELOC) is a debt solution that’s only available to Virginia homeowners. If you have equity available in your home, you can borrow against that equity and use the funds to pay off your debt. However, this can be a risky option for paying off credit card debt if you are living paycheck-to-paycheck. Home equity lending products put consumers at risk of foreclosure if they can’t make the payments. If you are considering borrowing against your home, call 1-800-435-2261 to speak with a HUD-certified housing counselor to make sure this is a safe option for you.

Nonprofit credit counseling services like those provided by Consolidated Credit help consumers identify the best solution for getting out of debt. This is a free service. Virginia residents can get a confidential debt and budget evaluation from a certified credit counselor. Then the counselor will explain options that are available to each person and recommend the best course of action based on an individual’s needs and goals.

If a Virginia consumer cannot get out of debt effectively on their own but has the ability to repay everything they owe to avoid bankruptcy, a debt management program is often the best solution. You enroll in the program through a credit counseling organization. They help you find a monthly payment you can afford and then work with your creditors to reduce or eliminate interest. Qualifying residents can get out of debt in 36-60 payments.

Debt settlement allows Virginia residents to get out of debt for a percentage of what they owe. You can settle debt on your own and negotiate with individual creditors and collectors or enroll in a debt settlement program to get professional help. This does cause credit damage. Each debt settled will be noted on your credit report for seven years from the date the account first became delinquent. However, it can be a viable debt relief option for avoiding bankruptcy when you are completely overwhelmed with debt.

If you’re curious how we can help you, below you will find a few case studies from clients that we’ve helped in Virginia residents. If you’re facing challenges with debt, call us at (844) 276-1544 to receive a free debt and budget evaluation from a certified credit counselor.

Ready to solve your problems with debt? Talk to a certified credit counselor for free to find the best way to get out of debt for you.

“It feels so good to have someone here to help me get my credit and my life back on track.

”

Where

she

started:

Total unsecured debt: $14,931.00

Estimated interest charges: $8,062.30

Time to payoff: 10 years, 6 months

Total monthly payments: $596.52

After DMP enrollment:

Average negotiated interest rate: 4.79%

Total interest charges: $1,990.03

Time to payoff: 4 years, 7 months

Total monthly payment: $309.00

Time Saved

5 years, 11 months

Monthly Savings

$287.52

Interest Saved

$6,072.27

Case Study

Maria

from

Lorton, VA

“If not for your persistence, I probably still wouldn’t be sleeping at night. It was hard at first, but when 2 or 3 of my credit cards were paid off it was an awesome feeling. Quick response and always there to assist. Thanks!

”

Where

she

started:

Total unsecured debt: $39,179.00

Estimated interest charges: $22,369.05

Time to payoff: 14 years, 3 months

Total monthly payments: $1,567.16

After DMP enrollment:

Average negotiated interest rate: 5.11%

Total interest charges: $1,920.78

Time to payoff: 4 years, 4 months

Total monthly payment: $798.00

Time Saved

9 years, 11 months

Monthly Savings

$769.16

Interest Saved

$20,448.27

Case Study

Justin

from

Charlottesville, VA

“Consolidated Credit has been instrumental in my recovery from debt and mistakes I made in the past. These folks are helpful and now my debt is almost gone!

”

Where

he

started:

Total unsecured debt: $15,578.00

Estimated interest charges: $8,467.97

Time to payoff: 12 years, 9 months

Total monthly payments: $626.28

After DMP enrollment:

Average negotiated interest rate: 9.20%

Total interest charges: $2,944.22

Time to payoff: 3 years, 10 months

Total monthly payment: $402.00

Time Saved

8 years, 11 months

Monthly Savings

$224.28

Interest Saved

$5,523.75

All articles and educational content on Consolidated Credit are written by and carefully reviewed by certified credit counselors, HUD-certified housing counselors and financial coaches.

Consolidated Credit follows strict sourcing guidelines and only links to reputable sources for information, such as government websites, credit bureaus, nonprofit organizations and reputable news outlets. We take every step possible to ensure all information comes solely from certified financial professionals.

If you feel that any of our content is inaccurate, out-of-date or otherwise questionable, please let us know through the feedback form on this page.