Learn how to make a budget that saves money and avoids debt.

Budgeting used to be a huge hassle, either sitting down with pen and paper or pulling out a spreadsheet. But these days, technology makes budgeting infinitely easier. You probably have access to a range of free tools that can help you track your spending daily. The right budgeting tool can help you save money, avoid debt, and maintain financial stability.

This section teaches you the basics of budgeting. These tips generally apply regardless of the budgeting strategy or tool you use.

How to Build a Budget that Fits Your Family

Learn about the basic building blocks of a budget and how you can use them to construct a solid foundation for your household finances.

A good budget provides a framework for financial stability and success. You build a stable money management structure that allows you to reach your financial goals. All of your monthly expenses should fit somewhere into that structure so you can avoid taking on high interest rate credit card debt for things that should be covered by cash.

Here’s a quick look at how a balanced budget works.

Building a budget starts by laying the foundation and adding up your total monthly income. Expenses should be separated between one of three levels – fixed, flexible and discretionary.

The first level is where all your needs with a fixed cost live. That’s any need with a cost that stays the same every month. The next level is where needs with no fixed cost live. In other words, things you can’t live without but the cost can vary from month to month. The final level is where your wants live. You know, the things that aren’t necessary but make life fun.

Credit card debt payments can live in one of two places in your budget, depending upon how much debt you have. If you have low balances and pay off what you charge at the end of every month then credit card payments live with those other flexible expenses. However, if you have large debts to pay off make big payments every month until you’ve paid it off in full.

Discretionary expenses are where all the fun and frills live in your budget. And this is where you should start if you need to make cuts to scale back. Savings often gets treated like a discretionary expense and shoved in with the rest of your wants, which means it can get lost in the mix or cut entirely. But really, savings should move in with your fixed expenses. Decide how much you can save each month and make that a set cost in your budget that you pay to yourself every month.

Once you’ve constructed a budget, you have to maintain it to make sure it stands up over time. Every few months compare your actual spending to what you planned to spend. This will make sure you’re keeping everything within the structure you set. This ensures that your financial house can hold all of your monthly expenses so credit cards don’t have to cover what’s been left out.

If you see you’re overspending consistently somewhere you may need to work on your budget again to make sure it’s not too bloated to fit the foundation. In some cases this may mean you have to cut something to make room. Eliminating debt or adding income will give you the ability to add these expenses back once you have room to fit them in.

For more advice about budgeting and managing money visit consolidatedcredit.org.

Now Playing

How to Build a Budget that Fits Your Family

Learn about the basic building blocks of a budget and how you can use them to construct a solid foundation for your household finances.

A good budget provides a framework for financial stability and success. You build a stable money management structure that allows you to reach your financial goals. All of your monthly expenses should fit somewhere into that structure so you can avoid taking on high interest rate credit card debt for things that should be covered by cash.

Here’s a quick look at how a balanced budget works.

Building a budget starts by laying the foundation and adding up your total monthly income. Expenses should be separated between one of three levels – fixed, flexible and discretionary.

The first level is where all your needs with a fixed cost live. That’s any need with a cost that stays the same every month. The next level is where needs with no fixed cost live. In other words, things you can’t live without but the cost can vary from month to month. The final level is where your wants live. You know, the things that aren’t necessary but make life fun.

Credit card debt payments can live in one of two places in your budget, depending upon how much debt you have. If you have low balances and pay off what you charge at the end of every month then credit card payments live with those other flexible expenses. However, if you have large debts to pay off make big payments every month until you’ve paid it off in full.

Discretionary expenses are where all the fun and frills live in your budget. And this is where you should start if you need to make cuts to scale back. Savings often gets treated like a discretionary expense and shoved in with the rest of your wants, which means it can get lost in the mix or cut entirely. But really, savings should move in with your fixed expenses. Decide how much you can save each month and make that a set cost in your budget that you pay to yourself every month.

Once you’ve constructed a budget, you have to maintain it to make sure it stands up over time. Every few months compare your actual spending to what you planned to spend. This will make sure you’re keeping everything within the structure you set. This ensures that your financial house can hold all of your monthly expenses so credit cards don’t have to cover what’s been left out.

If you see you’re overspending consistently somewhere you may need to work on your budget again to make sure it’s not too bloated to fit the foundation. In some cases this may mean you have to cut something to make room. Eliminating debt or adding income will give you the ability to add these expenses back once you have room to fit them in.

For more advice about budgeting and managing money visit consolidatedcredit.org.

Up Next

Balance Your Budget to Stop Living Paycheck-to-Paycheck

There’s an easy way to ensure you always maintain a balanced budget. Learn how to use your income-to-expense ratio to balance your budget so you can stop living paycheck-to-paycheck.

Balancing your budget so you can stop living paycheck to paycheck

A balanced budget ensures that all of your various expenses can fit the foundation of your income, so you can maintain a stable house through any challenge. But what’s the right balance for your budget structure?

When you live paycheck to paycheck your income barely fits all of your expenses. In order to create balance, you’ll need to check your income-to-expense ratio.

Divide your total monthly expenses by your total monthly income. Your ratio should be less than 1, indicating that you spend less than you earn. Ideally, your ratio should be point-seven-five or less. This means that you spend less than 75% of your income, which leaves 25% of your income as free cash flow in your budget.

Some of your cash flow can be converted into savings. This helps you increase the amount you dedicate to save, so you can have a robust, solid saving strategy that supports your goals. Ideally, savings should be treated like a regular reoccurring expense in your budget. This means savings gets housed with the rest of your fixed expenses. Aim to save at least five to ten percent of your income each month.

This is beneficial because unexpected expenses always seem to show up. When a large expense arrives unannounced, it has the potential to throw your financial house out of balance. But free cash flow and savings help you accommodate unexpected expenses easily. That way, you don’t have to invite credit card debt in for unexpected costs, because credit card debt shouldn’t be a welcome solution to address budget challenges.

For more great budgeting advice, visit ConsolidatedCredit.org.

Organizing Your Expenses So It’s Easy to Cut Back

Learn why dividing your expenses into the three categories we recommend – fixed, flexible and discretionary – makes it easy to cut back so you have more free cash flow to save and pay off debt.

Organizing your budget effectively to maintain stability. A good budget categorizes expenses, keeping them organized.

The base level of your budget houses fixed expenses. These expenses come first because they’re things you need to survive. This includes rent or mortgage payments, HOA fees, insurance, student loans and car payments. The cost for each fixed expense generally stays the same. However, changes may occur annually. But beyond these annual changes, fixed expenses are usually easy to plan around.

The next level of your budget houses all of your flexible expenses. Flexible expenses are also things you may need to survive, but they have no set cost. As a result, they can get too big to fit into your budget unless you monitor them closely to avoid overspending. This can make flexible expenses trickier to manage because they fluctuate. And some months certain flexible expenses may not show up at all. While it can be harder to control these expenses, they’re also easier to trim down if you need to cut back.

Finally, the top level of your budget is where all the nice-to-haves live. This is your discretionary expenses. This level includes everything from entertainment and subscriptions to tithes and trips to the gym or salon. As tough as it can be to kick these out, you can live without them, if necessary.

As you take stock of discretionary expenses take note of every incidental that may be hiding out. This includes things like your “cappuccino” factor – that’s the $3.50 you spend on specialty coffee each morning. That expense may not seem like much, but it adds up to nearly $1,300 a year! So take note of these small incidentals to make sure they fit in your budget and if they don’t, they have to go.

For more advice on budgeting, visit ConsolidatedCredit.org.

The Secret to Managing Debt within Your Budget

Credit card debt can be tough to manage because it can act like a fixed or flexible expense, depending on how you manage debt. Learn the right way to use your budget when you need to pay off credit card debt.

Using your budget to strategically manage debt.

A solid budget structure makes it easy to control debt. Most debts are housed with your other fixed expenses – like your mortgage or auto loan are installment debts with fixed payments.

But credit card debt can be a little tricky to house. Credit cards are revolving debt. This means your bill grows as your balances go up. But if you have zero balance, then that bill disappears completely.

If you pay off your debts in-full each month, then credit card debt gets counted as a flexible expense. But if you carry balances over each month, then you may be better off making credit card debt payments as a fixed expense. This means you have to consider your budget as a whole to see how much you can afford to pay.

First, see how much you can afford to pay each month. You evaluate your free cash flow, to maximize the amount of money you have for debt repayment. Then you set this amount as a fixed expense in your budget. The funds are used to pay off one credit card debt at a time, starting with the card that has the highest APR.

So, if you have five credit cards to pay off, you make minimum payments on all four. Then use the rest of your funds to make the biggest payment possible on the debt with the highest APR. Once that debt is gone, you move on to the next. And you continue to pay each debt down one at a time.

If you don’t have much free cash to start with, knock out your debts starting with the lowest balance. Each debt you knock out frees up more cash to focus on the next. In normal circumstances, credit card debt payments should take up to no more than ten percent of your income.

And remember, if you’re having trouble making debt payments fit in your budget, Consolidated Credit is here to help.

Analyzing and Adjusting Your Budget

Your budget is never static! Learn how to regularly analyze your budget to make sure you stay on track and how to adjust your budget for changes major life changes and seasonal expenses.

Analyzing and adjusting your budget to foster financial stability.

A budget is a basic blueprint of your finances. It helps you organize and categorize expenses for a stable financial house. But you can’t just draw it up and toss it aside. You have to check in often and make adjustments as needed.

Fixed expenses only adjust if there’s a change, for example annual property tax adjustments on your mortgage. This consistency makes it easy to house fixed expenses.

On the other hand, flexible and discretionary expenses have no set cost. So you have to take steps to ensure they fit in your budget structure. To do this, you set target spending limits for each expense. Look back at what you spent in the last three months. Then take an average of those three months to determine a target spending limit.

Once your budget is set, compare your actual spending to the targets you set. If actual spending is consistently higher, you must cut back or adjust the target limit. Just make sure total expenses always fit the structure based on your income. If one expense grows, something else may need to be reduced or cut.

Come back to review your budget at least once per quarter or every three months. And also remember to make seasonal adjustments. Utility bills and fuel costs typically change from summer to winter. And you can also use your budget to plan ahead for key events like back to school and holiday shopping. By revisiting your budget often, you can always have a financial house that adjusts as needed to fit your life and goals.

For more great tips on budgeting, visit ConsolidatedCredit.org

If you have questions or need help balancing your budget because of debt, call (844) 276-1544 or request a consultation online.

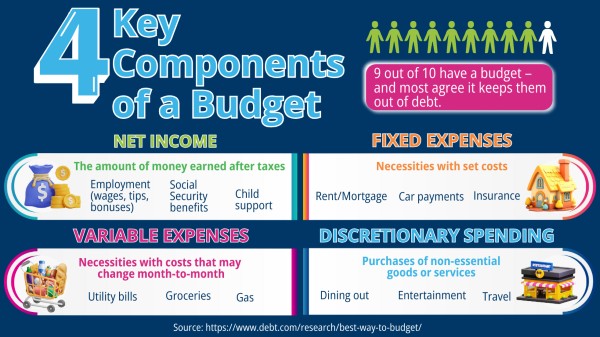

There are four basic elements that make up any household budget:

Income

Fixed expenses

Flexible expenses

Discretionary expenses

Income isn’t just limited to money you receive from paychecks. It can also include government benefits, alimony or child support, and even returns on investments.

Every budget also has three basic types of expenses. Fixed expenses and flexible expenses are both necessities. Fixed expenses, like mortgage or rent payments and insurance, have a set cost that stays the same every month. Flexible expenses, like groceries or your electric bill, vary month to month.

Discretionary expenses cover your wants. They also tend to have costs that change from month to month, but not always. For instance, a Netflix subscription has a consistent cost, but it’s not a necessity. A good budget should always keep wants separate, so it’s easier to cut back if you see you’re overspending.

Types of expenses vs. categories

Most budgeting tools don’t break up purchases by those three types of expenses. Instead, they categorize your expenses. So, the tool may automatically separate out food transactions and fuel transactions. Categories of expenses can be helpful for setting target spending limits. But you should still keep types of expenses in mind.

For instance, we recommend dividing your food budget into two separate categories: groceries and dining out. Groceries are a flexible expense because food is a necessity. But eating out is a luxury and tends to cost more. So, if you make dining out a separate category, you maintain a budget that keeps your needs and wants separate.

How to balance your budget

A good personal budget prevents overspending by balancing expenses versus income. But it’s not just about keeping total expenses below your total income. If you spend every dollar you earn, that doesn’t make you financially stable. A balanced budget has built-in money for saving, leaving some breathing room for unexpected expenses. This is known as “free cash flow.”

In order to maintain financial stability, you should only spend about 75% of what you earn. Your income-to-expense ratio should be 1.25 or greater.

If you live paycheck-to-paycheck, talk to a certified credit counselor today for a free debt and budget evaluation.

Personal budgeting only works if you use it consistently. If you make your budget and then ignore it, you will probably overspend. Overspending usually leads to credit card debt because you pull out the plastic to cover gaps in your budget.

How to maintain and adjust your budget

Budgets are not set in stone. In fact, they fluctuate throughout the year and as your needs change. This means you need to regularly adjust your budget to suit your needs and seasonal expenses. You also need to adjust your budget anytime there is a change in your financial situation. If you lose your job, get a raise, take a pay cut, or add a new expense, you should revisit your budget. That way, you can adjust it accordingly and maintain financial stability.

Separating monthly savings from cash flow

One mistake people often make in budgeting is how they treat savings. Some people think savings is the same as free cash flow — i.e., you save whatever you have left at the end of the month. But this is a good way never to save anything!

Instead, you should treat savings as a fixed expense. You see how much you can afford to save each month – ideally, 5-10% of your income. Then, you set that amount as a fixed expense. It’s like a bill that you pay yourself each month.

If you keep that 5-10% separate from the 25% of your income that you maintain for free cash flow, you protect your savings. This ensures that you don’t drain your emergency savings each month on those unexpected expenses that inevitably come up.

Using a personal budget to manage debt

Another way budgeting helps you is by making it easier to manage debt. Debts generally fall into one or two categories, depending on your financial situation. Debts like mortgages and car payments are always fixed. However, credit card debt can be fixed or flexible. Paying off any charges you make in full every month tends to be a flexible expense. However, if you have balances to pay off, making the payments a fixed expense is often better.

Where to find the right budgeting tool

There are plenty of ways that you can gain access to good budgeting tools for free. Or, if you prefer, you can pay for software or an online platform if it suits your needs.

Check your checking account first. Many banks and credit unions offer a free budgeting tool as part of their online and mobile banking platforms. This can be beneficial since it’s already integrated with your main account.

Look online or in your app store. There are plenty of free budgeting tools available online or in the app store for your favorite mobile device. Just make sure they’re well-reviewed and secure, since you will need to link it up to your financial accounts.

Use desktop budgeting software. If you’re concerned about the risk of unauthorized access online, find budgeting software for your home desktop. This will help you budget without increasing your risk.

If none of those options suit your needs and goals, then you can go old-school. Either do pen-and-paper budgeting or build your own spreadsheet. We offer some free worksheets that can help you get started:

Special events throughout the year, like holidays and vacations, can bust your budget. One-off expenses, including gifts, decorations, party planning, and travel, can quickly stack up and lead to overspending. These expenses often end up on high-interest-rate credit cards, increasing the balances you need to pay off. Creating spending plans for these special events can help you avoid overspending and excess credit card debt.

Vacation Budget Planner

A 2024 Bankrate survey found that 1 in 3 Americans who plan to travel this year “plan to go into debt to pay for travel.” Use our free vacation budget planner to plan an affordable vacation that won’t lead to credit card debt.

The back-to-school shopping season is the second most expensive time of the year for families. The average cost is $875. This guide can help you build a back-to-school budget that won’t lead to overspending and credit card debt.

If the winter holiday shopping season always leads to a mountain of credit card debt for you, you’re not alone. The average family spends over $1,000 to make the season merry and bright. Use Consolidated Credit’s holiday survival guide to set a holiday budget that won’t break the bank as you bring your family and friends joy.

Valentine’s Day is the third most expensive holiday for most consumers (after Christmas and Mother’s Day). The average Valentine’s Day shopper shells out roughly $186 to spread the love. Our Valentine’s Day Spending Planner can help you stay on budget.

College students don’t usually take the time to budget. That’s a mistake, especially if you have a credit card with you during your school years. It’s easy to forget how much you’re spending if you don’t keep a budget and track your finances. That’s how college students fall further into debt and end up not saving money for the future.

With the unruly nature of our economic times, getting your kids involved with budgeting is wise. Teaching your children the value of a hard-earned dollar and understanding the consequences of overspending are valuable life lessons that can carry them through their lives. Budgeting will give them the groundwork they need to begin a life of sound financial decisions.

Success Story

Kasey L. from Las Vegas, NV

“Approximately three years ago, my husband and I were in a lot of financial debt. We had multiple collections, lots of little accounts, and other bills that became too overwhelming to manage on our own.

Consolidated handled all of our accounts and managed to reduce our minimum payments, almost eliminated all of our interest, and ultimately helped me to pay off all of my debt. They were professional and friendly throughout the entire experience.

Three years later I am happy to announce that we are debt free and we just purchased our first home! We could not have done it without Consolidated! I would recommend them to anyone who is feeling overwhelmed by their finances. Thank you!

”

Success Story

Bruce D. from Derry, NH

“We have had good experiences with Consolidated Credit, it has really helped learning to control our spending habits and get our financial house in order.

”

All articles and educational content on Consolidated Credit are written by and carefully reviewed by certified credit counselors, HUD-certified housing counselors and financial coaches.

Consolidated Credit follows strict sourcing guidelines and only links to reputable sources for information, such as government websites, credit bureaus, nonprofit organizations and reputable news outlets. We take every step possible to ensure all information comes solely from certified financial professionals.

If you feel that any of our content is inaccurate, out-of-date or otherwise questionable, please let us know through the feedback form on this page.